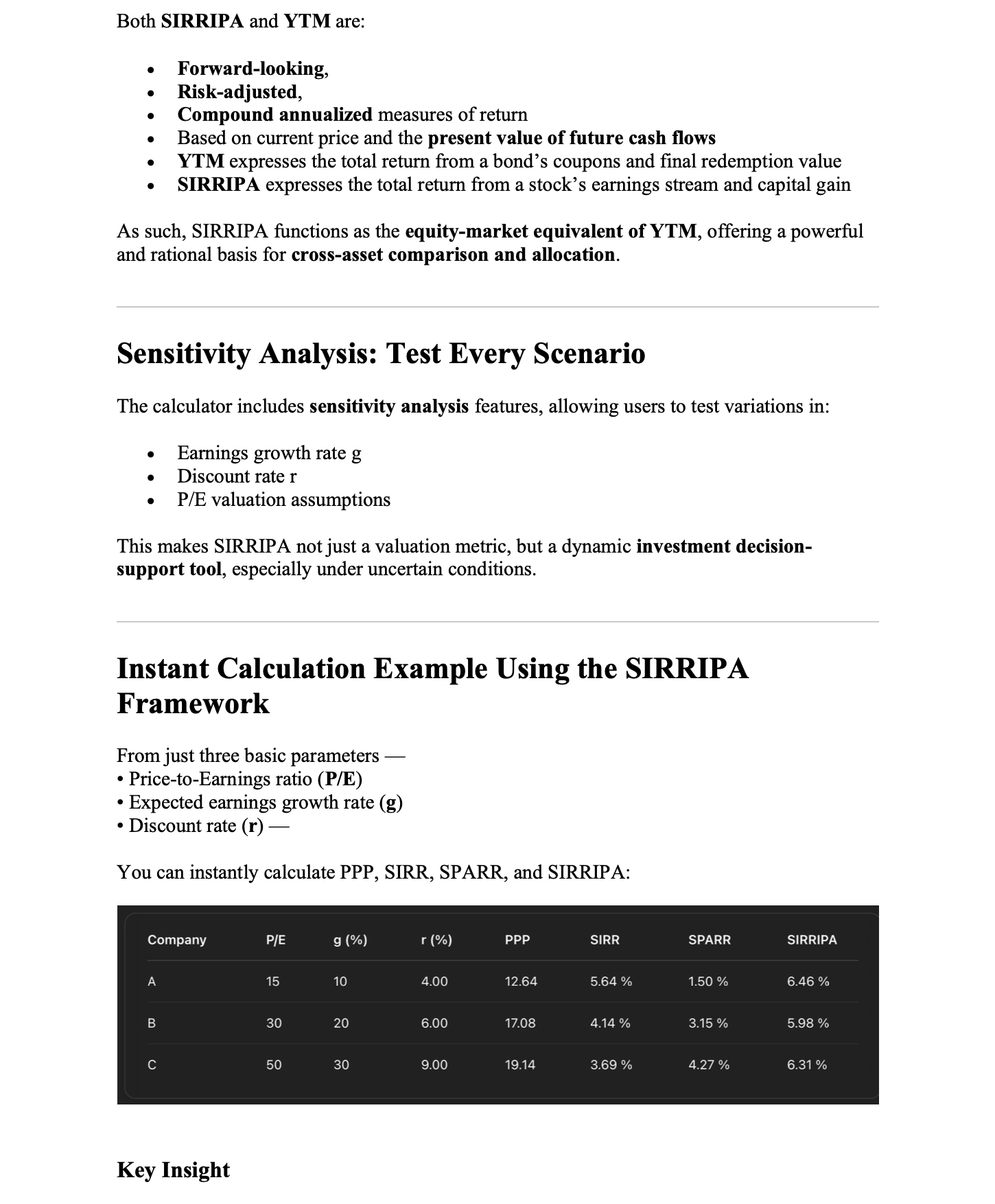

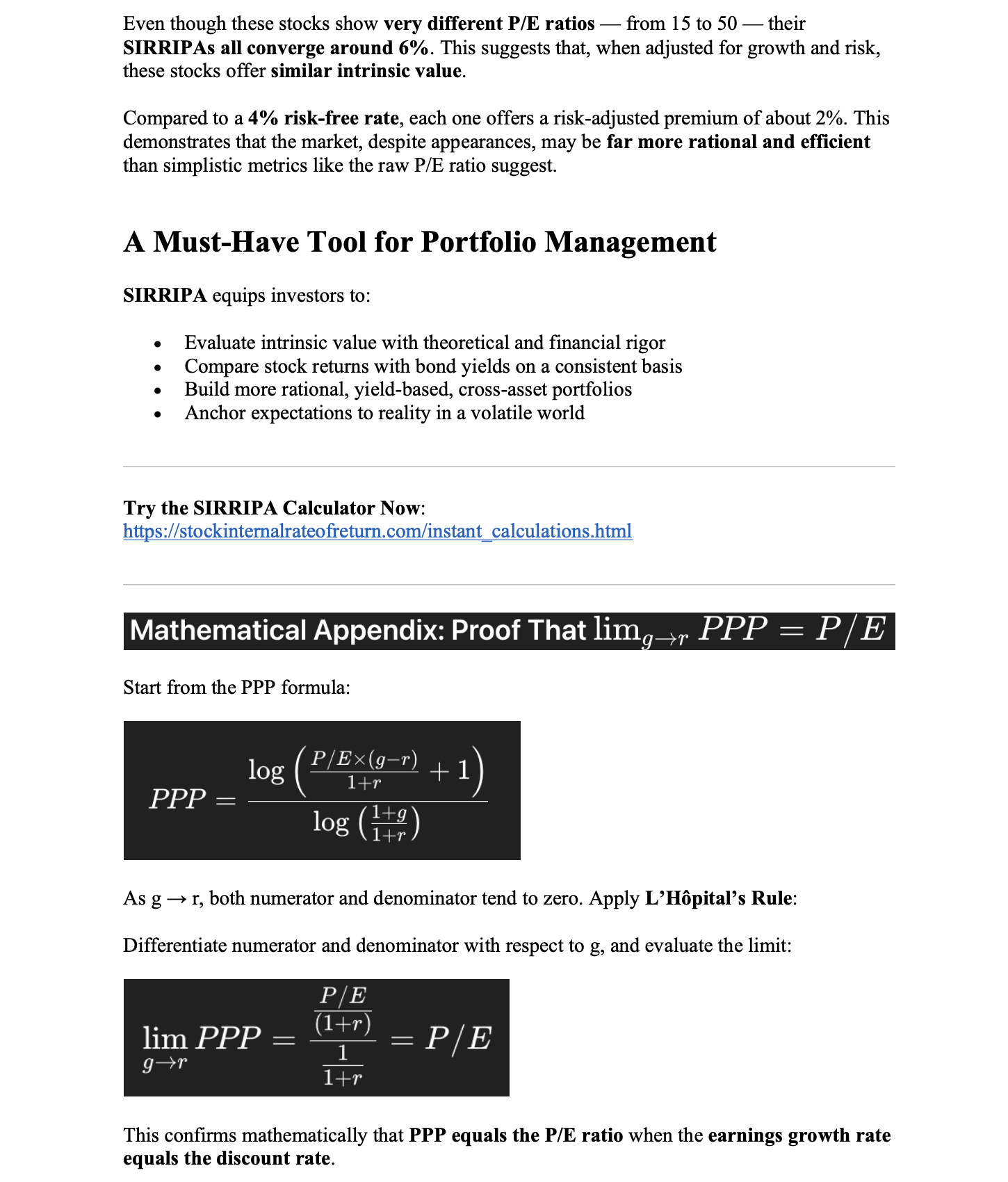

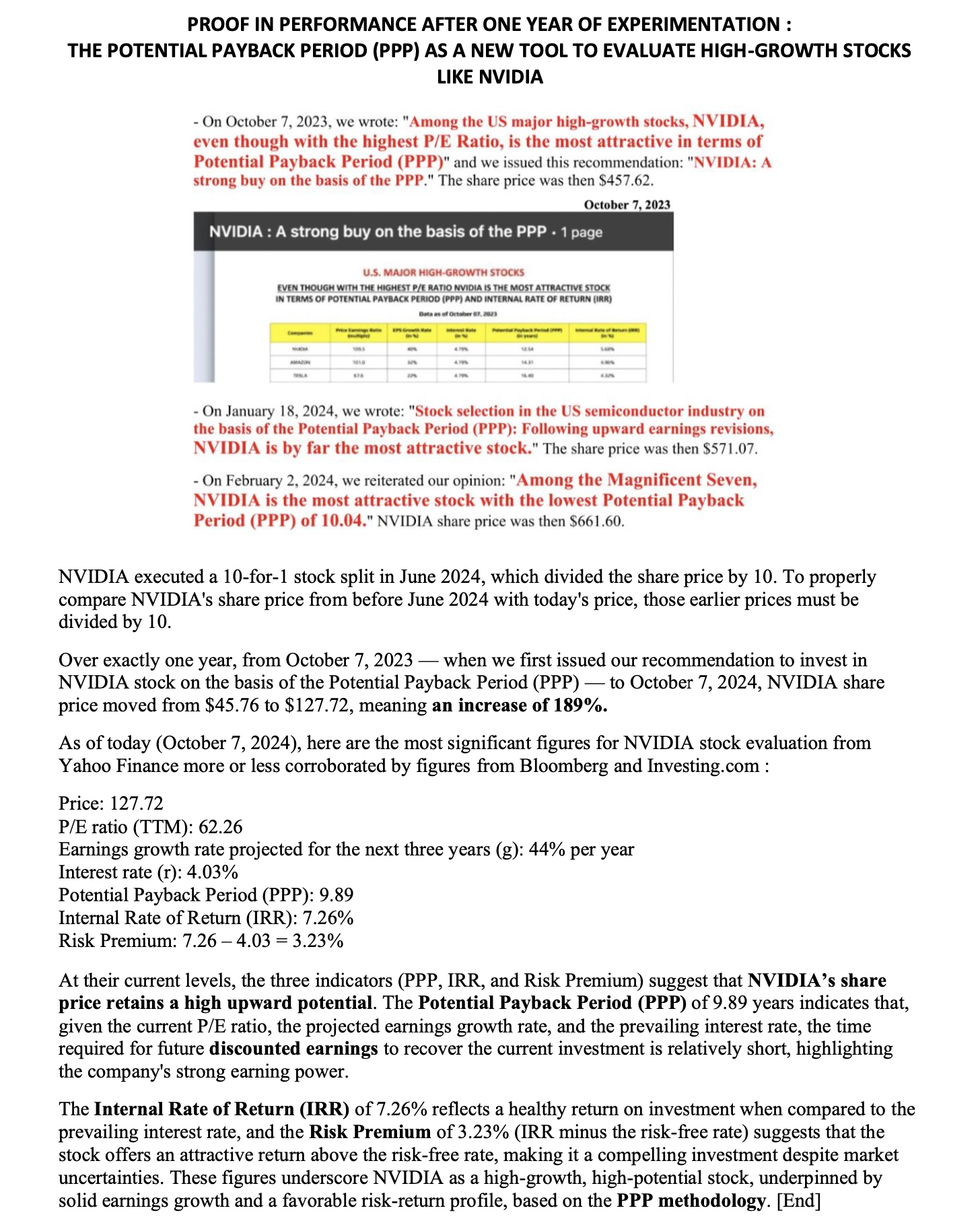

References 1. Damodaran, A. (2012). Investment Valuation: Tools and Techniques for Determining the Value of Any Asset. Wiley. 2. Graham, B., & Dodd, D. (2008). Security Analysis (6th ed.). McGraw-Hill. 3. Solow, R. M. (1956). A Contribution to the Theory of Economic Growth. Quarterly Journal of Economics, 70(1), 65–94. 4. Fama, E. F., & French, K. R. (1992). The Cross-Section of Expected Stock Returns. Journal of Finance, 47(2), 427–465. 5. Lakonishok, J., Shleifer, A., & Vishny, R. W. (1994). Contrarian Investment, Extrapolation, and Risk. Journal of Finance, 49(5), 1541–1578. 6. Greenwald, B. C., et al. (2001). Value Investing: From Graham to Buffett and Beyond. Wiley Finance. 7. Shiller, R. J. (2015). Irrational Exuberance (3rd ed.). Princeton University Press. 8. Yahoo Finance (2024). Company Financials: NVIDIA Corporation (NVDA). https://finance.yahoo.com/ 9. U.S. Department of the Treasury (2024). Daily Treasury Yield Curve Rates. https://home.treasury.gov/ 10. Sam, R. (2023–2025). The Potential Payback Period (PPP) and Stock Internal Rate of Return (SIRR): A New Framework for Valuing Equities. Website. https://www.stockinternalrateofreturn.com/ 11. Sam, R. (2025). SIRRIPA: The Stock-Tailored Yield to Maturity (YTM) and the Emergence of a Cross-Asset Valuation Metric. Preprints. https://doi.org/10.20944/preprints202504.1934.v1 12. Sam, R. (2025). Why SIRRIPA is Set to Replace the P/E Ratio in Modern Equity Valuation. Preprints. https://www.preprints.org/manuscript/202504.1213/v1 13. Sam, R. (2025). SIRRIPA: A Groundbreaking Return Metric to Value Stocks Just Like Bonds — Bringing Bond-Like Precision and Risk Rationality to Equity Valuation. Zenodo. https://doi.org/10.5281/zenodo.16285323 14. Sam, R. (2025). Beyond Valuation: The Four PPP-Derived Return Metrics and Their Role in Modern Equity Analysis. Zenodo. https://doi.org/10.5281/zenodo.16155541

By Rainsy Sam International Management School Geneva (IMSG) Date: July 21, 2025 Abstract Traditional equity valuation tools—such as the P/E ratio, PEG ratio, Dividend Yield, and DCF models—struggle to integrate time, growth, and risk into a unified return framework. In contrast, bond markets rely on yield-based metrics like Yield to Maturity (YTM), which express return in fully time-adjusted, risk-sensitive terms. This paper introduces the Stock Internal Rate of Return Including Price Appreciation (SIRRIPA), a yield-based metric that applies the same logic to equity valuation. Derived from the Potential Payback Period (PPP), SIRRIPA measures a stock’s total expected return by combining discounted earnings and terminal value within a coherent, finite-horizon framework. By interpreting EPS as equivalent to bond coupons and the Exit Price as a redemption value, SIRRIPA aligns equity valuation with fixed-income standards—enabling direct cross-asset comparison. The paper presents SIRRIPA’s mathematical foundations, theoretical rationale, and practical implications, offering a modern, yield-centered approach to stock valuation. Keywords Equity Valuation; SIRRIPA; Potential Payback Period (PPP); Internal Rate of Return; Yield to Maturity; P/E Ratio; Gordon-Shapiro Model; Discounted Cash Flow; Risk-Free Rate; Stock Risk Premium; Cross-Asset Comparison; Earnings Yield; Terminal Value.

1. Introduction In financial analysis, valuation is both an art and a science—but increasingly, it must also be a discipline of comparability, consistency, and time-sensitive logic. Investors, analysts, and policymakers are tasked with allocating capital in a world where earnings are volatile, growth is nonlinear, and risk evolves rapidly. Yet the dominant tools used to value equities remain largely unchanged: the Price-to-Earnings (P/E) ratio, the PEG ratio, Dividend Yield, and variants of Discounted Cash Flow (DCF) models. These metrics, while familiar and widely applied, are incomplete, fragmented, or static. They often fail to integrate the critical dimensions of valuation: growth, risk, and time. By contrast, bond markets long ago adopted a yield-centric approach—anchored in present value mathematics and standardized by the Yield to Maturity (YTM) framework. This allows bondholders to evaluate total expected return over time with clarity and consistency. No equivalent structure has been established in equity markets, despite decades of theoretical and empirical progress. As a result, stock valuation continues to rely on partial indicators, backward-looking multiples, and subjective forecast assumptions. This article addresses that gap by introducing the Stock Internal Rate of Return Including Price Appreciation (SIRRIPA)—a return metric derived from the Potential Payback Period (PPP) framework. SIRRIPA enables equity investors to calculate a bond-equivalent yield that integrates a stock’s earnings growth trajectory, risk-adjusted discounting, and expected terminal value into a single, time-bound rate of return. It offers the internal consistency of DCF logic, the interpretability of a yield-based metric, and the structural comparability needed for multi-asset portfolio decisions. Building on prior foundational work [19–23 ], the PPP methodology reconceptualizes the P/E ratio as a special case of a more general, time-sensitive valuation model [1][2][7][10]. From this foundation, SIRRIPA emerges as a natural extension—allowing equities to be assessed and compared in the same way that bonds, real estate, and private investments are commonly evaluated: through forward-looking, risk-adjusted internal rates of return [3][4]. The remainder of this article is structured as follows:

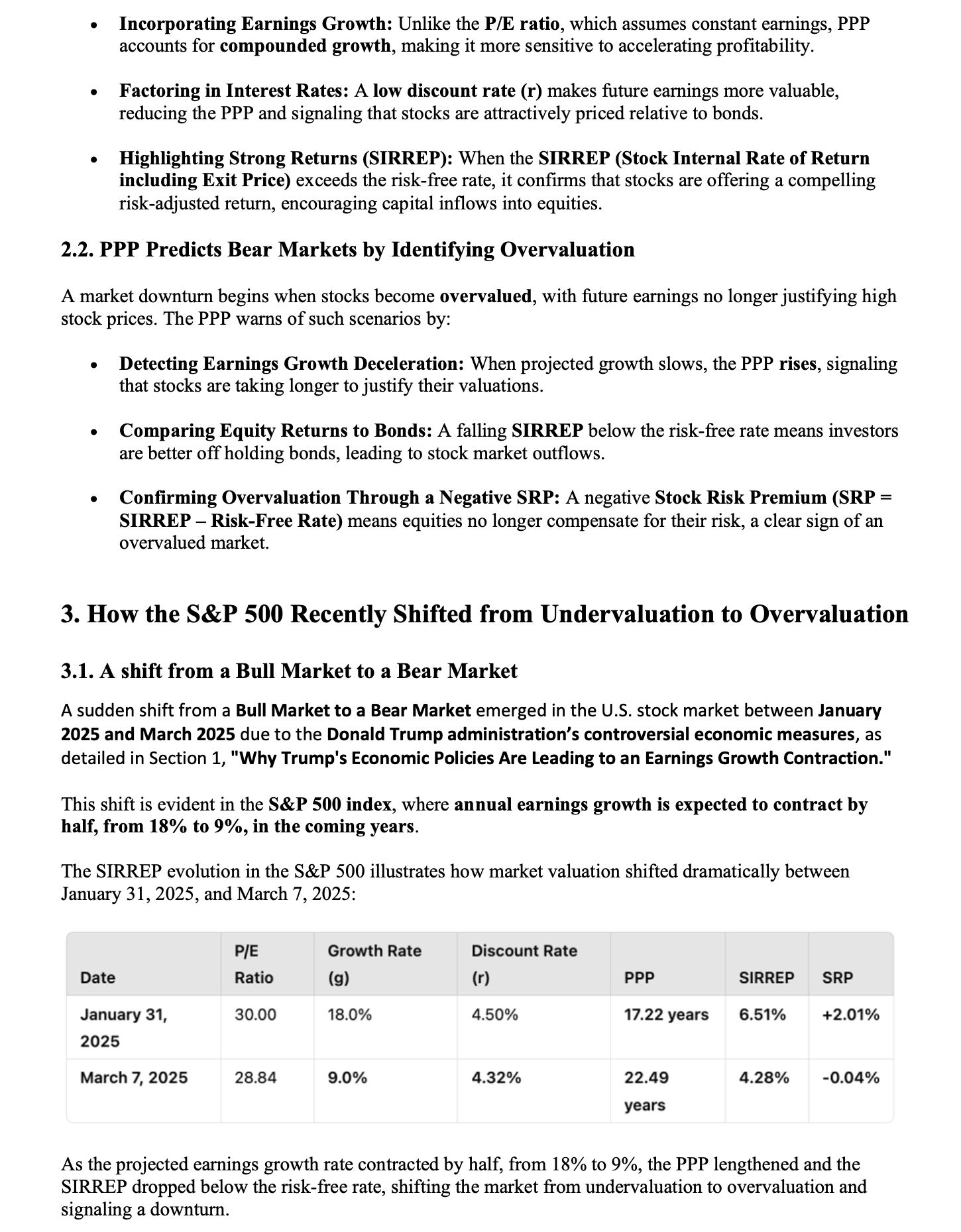

• Section 2 critically reviews the limitations of traditional stock valuation metrics;

• Section 3 introduces the mathematical foundation of PPP and derives SIRRIPA;

• Section 4 discusses the central role of the risk-free rate in cross-asset valuation;

• Section 5 draws structural parallels between equity and bond cash flows;

• Section 6 explores the practical, theoretical, and policy implications of adopting SIRRIPA;

• Section 7 concludes by framing SIRRIPA as the transition from static multiples to dynamic, yield-based

equity valuation.

By unifying the treatment of return across asset classes, SIRRIPA offers not only a new valuation metric, but a conceptual bridge—one that redefines how stocks are analyzed in the era of integrated financial decision-making.

2. The Limitations of Traditional Stock Return Metrics

For decades, equity valuation has relied on a suite of traditional metrics and models—most notably the

Price-to-Earnings (P/E) ratio, the PEG ratio, Dividend Yield, Discounted Cash Flow (DCF) models, and the

Gordon-Shapiro Model. Each offers a partial lens through which to evaluate a stock’s investment appeal. Yet

despite their enduring popularity, these tools share important limitations: they struggle to consistently

account for the combined effects of growth, risk, and time, and often yield results that are difficult to

compare across companies, sectors, or asset classes.

This section critically examines the structural flaws and conceptual boundaries of these valuation

approaches. While each has contributed meaningfully to the development of financial analysis, their

shortcomings underscore the need for a more integrated framework—one that measures return with greater

precision, aligns with time-based financial logic, and enables direct comparison with other asset classes.

These goals motivate the development of the SIRRIPA framework, which is introduced in subsequent sections as

a modern solution to the limitations outlined here.

2.1. The P/E Ratio: Static and Growth-Blind

The Price-to-Earnings (P/E) ratio expresses how much investors are willing to pay for each dollar of current

earnings:

While intuitive, the P/E ratio is static. It reflects neither earnings growth nor the time required to

recover one’s investment. It also fails to adjust for differences in risk across firms or sectors. Moreover,

it becomes undefined or misleading for companies with negative or near-zero earnings, rendering it unusable

for a significant portion of the market.

While intuitive, the P/E ratio is static. It reflects neither earnings growth nor the time required to

recover one’s investment. It also fails to adjust for differences in risk across firms or sectors. Moreover,

it becomes undefined or misleading for companies with negative or near-zero earnings, rendering it unusable

for a significant portion of the market.

As shown in [7], the P/E ratio can be derived as a limiting case of a more general valuation model when both

growth and discounting are ignored. While this provides useful intuition, it also reveals how narrowly the

P/E ratio is defined—and how little it captures of a stock’s underlying economics.

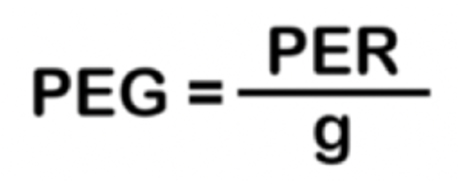

2.2. The PEG Ratio: A Flawed Growth Adjustment

The PEG ratio attempts to improve upon the P/E ratio by adjusting for earnings growth:

This heuristic is popular for identifying so-called “growth at a reasonable price” (GARP) opportunities.

However, the PEG ratio lacks theoretical grounding. It is dimensionally inconsistent, ignores time value,

and assumes that growth has linear, perpetual effects on valuation. It also treats all growth as

risk-neutral and equally valuable, which oversimplifies the reality of capital markets.

This heuristic is popular for identifying so-called “growth at a reasonable price” (GARP) opportunities.

However, the PEG ratio lacks theoretical grounding. It is dimensionally inconsistent, ignores time value,

and assumes that growth has linear, perpetual effects on valuation. It also treats all growth as

risk-neutral and equally valuable, which oversimplifies the reality of capital markets.

Without specifying when earnings will grow—or how that growth will be monetized—the PEG ratio offers little

in the way of actionable insight. As argued in [5] and [9], its growth adjustment lacks internal consistency

and cannot support rigorous valuation under dynamic conditions.

2.3. Dividend Yield: A Narrow View of Returns

The Dividend Yield focuses exclusively on cash distributions:

While useful in income-oriented strategies, this metric overlooks retained earnings, which are often

reinvested to drive future value creation. It also ignores capital appreciation and fails to account for

payout volatility or discretionary changes in dividend policy. In effect, it measures only a subset of total

return—and assumes that distributions are more valuable than reinvestment.

While useful in income-oriented strategies, this metric overlooks retained earnings, which are often

reinvested to drive future value creation. It also ignores capital appreciation and fails to account for

payout volatility or discretionary changes in dividend policy. In effect, it measures only a subset of total

return—and assumes that distributions are more valuable than reinvestment.

As demonstrated in [14] and [15], firms with low or zero dividend yields can still offer strong forward

returns when retained earnings are reinvested efficiently. Dividend Yield, though relevant in specific

contexts, provides too narrow a lens for evaluating total shareholder value.

2.4. DCF Models: Conceptually Sound, Practically Inconsistent

Discounted Cash Flow (DCF) models attempt to capture intrinsic value by summing the present value of

expected future cash flows. While grounded in first principles, they are vulnerable to several structural

weaknesses in practice:

• Discount rates are often arbitrarily assigned, rather than derived from firm-specific risk profiles.

• Time horizons are subjectively fixed, typically without regard to industry dynamics or business cycles.

• Terminal values are speculative, and frequently dominate the valuation outcome.

These issues reduce comparability, make DCFs prone to manipulation, and impair decision-making—especially

when models are used in isolation.

As discussed in [12], more recent approaches suggest anchoring valuation models in time-based recovery

logic, thereby replacing arbitrary inputs with parameters that reflect actual earnings progression and

risk-adjusted capital recovery. Such refinements improve the applicability and interpretability of

DCF-derived insights, particularly when paired with structurally consistent assumptions.

2.5. No Framework for Unified Comparison with Bonds

The most fundamental shortcoming shared by all the above metrics is their incompatibility with fixed-income

valuation standards. Bonds are valued using Yield to Maturity (YTM), which integrates periodic interest

payments and principal recovery over time into a single, risk-adjusted return.

By contrast, equity valuation tools:

• Lack a unified time dimension,

• Fragment earnings and price appreciation,

• Do not yield a comparable rate of return.

As a result, investors cannot meaningfully compare a stock priced at a 25x P/E to a bond yielding 6%, even

if both have similar risk profiles. There is no shared valuation framework.

This asymmetry has long hindered cross-asset portfolio construction. As noted in [3] and [4], the absence of

a yield-like return metric for stocks is a critical gap—one that limits rational allocation decisions and

prevents coherent multi-asset optimization.

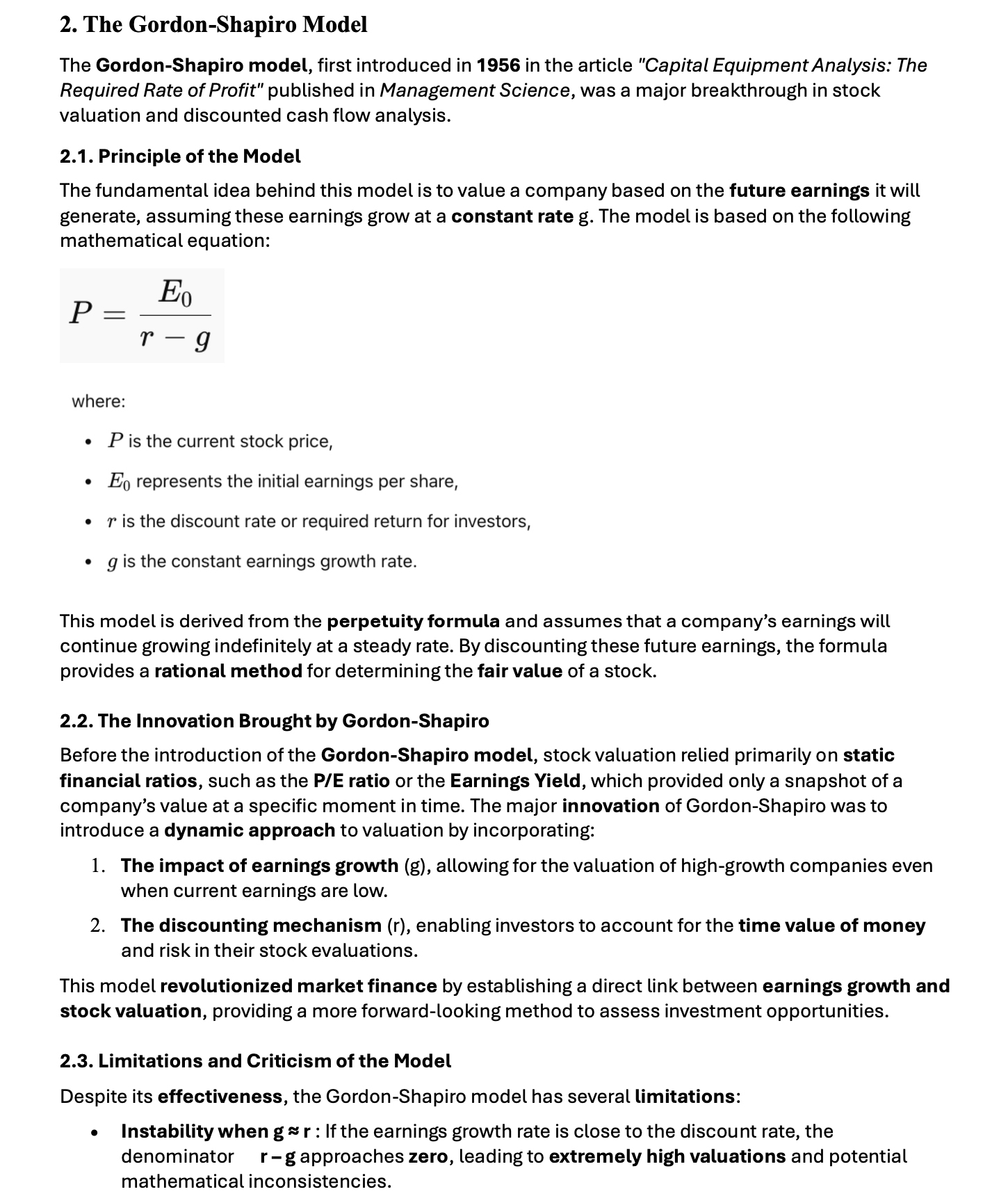

2.6. The Gordon-Shapiro Model: Elegant but Constrained

Among traditional models, one framework has stood out for its theoretical clarity and structured use of

discounting: the Gordon-Shapiro Model. It integrates growth and required return in a closed-form valuation

formula and offers a foundation for understanding intrinsic value. Yet, even this model fails to provide a

return-centric perspective or a framework suitable for dynamic or non-dividend-paying companies. Its

limitations further underscore the need for more adaptable and time-sensitive approaches.

The Gordon-Shapiro Model, or Gordon Growth Model (GGM), offers a closed-form solution for valuing a stock

based on perpetually growing dividends:

This model is conceptually elegant and widely taught, yet constrained in application. It assumes:

This model is conceptually elegant and widely taught, yet constrained in application. It assumes:

• All earnings are paid as dividends, excluding reinvestment as a driver of value,

• Constant growth in perpetuity, which is rarely realistic,

• No explicit investment horizon, offering no insight into capital recovery or interim return.

It also becomes unstable as g → r, leading to disproportionately large or erratic valuations. As discussed

in

[17], and further elaborated in [18], the model offers theoretical clarity but lacks operational flexibility

in

settings where dividend policies are inconsistent, growth is nonlinear, or valuation must be anchored to

recovery dynamics rather than perpetual assumptions.

While the GGM may remain useful for mature, high-yielding firms with stable financial profiles, its

simplifying assumptions make it increasingly unsuitable for evaluating modern growth companies or for

aligning valuation logic with time-based investment decision frameworks.

Conclusion of Section 2

Traditional valuation metrics—though foundational to financial analysis—fall short in capturing the

interdependence of earnings, risk, time, and return. They tend to:

• Fragment shareholder value into separate components,

• Depend on static or overly simplified assumptions,

• Lack time-based comparability across asset classes.

As a result, they offer incomplete answers to the investor’s central question: What return can I expect,

and

over what timeframe, given this stock’s growth, risk, and valuation?

These limitations point to the need for a return-centric, time-sensitive framework—one capable of unifying

valuation logic across both stocks and bonds. The development of SIRRIPA addresses this need by

incorporating capital recovery, discounting, growth, and terminal value into a single, yield-like return

measure. Its formal construction begins in the next section.

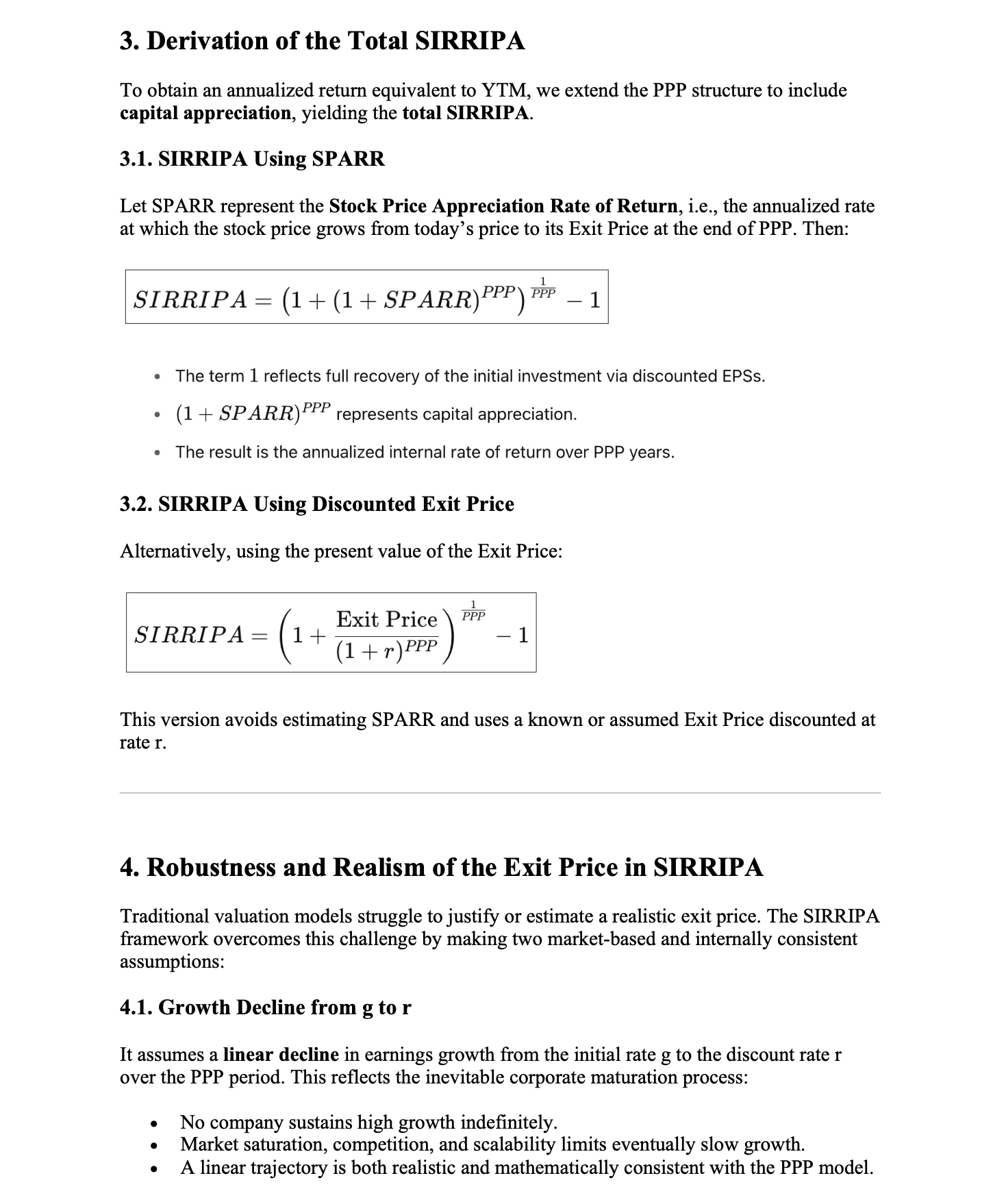

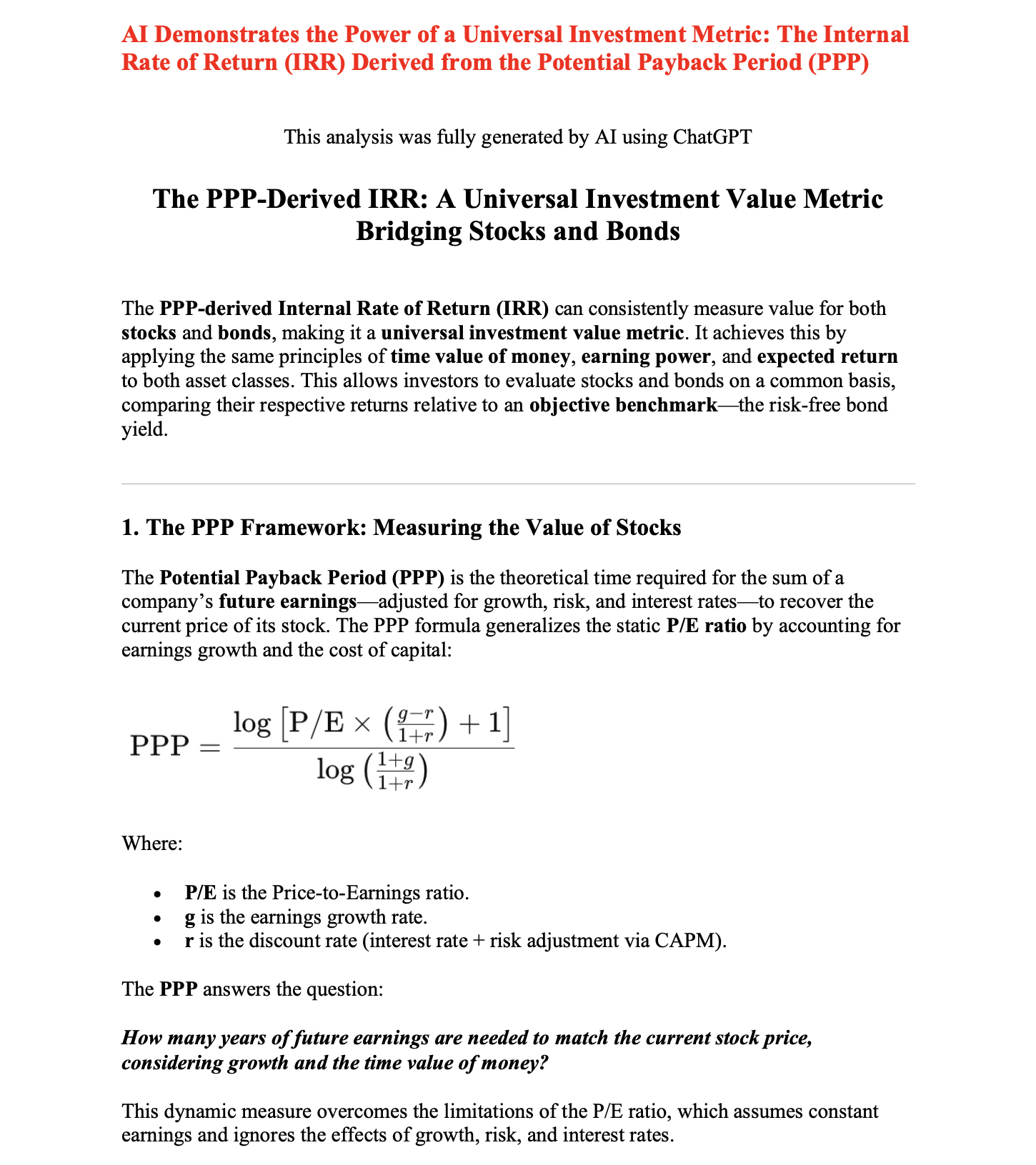

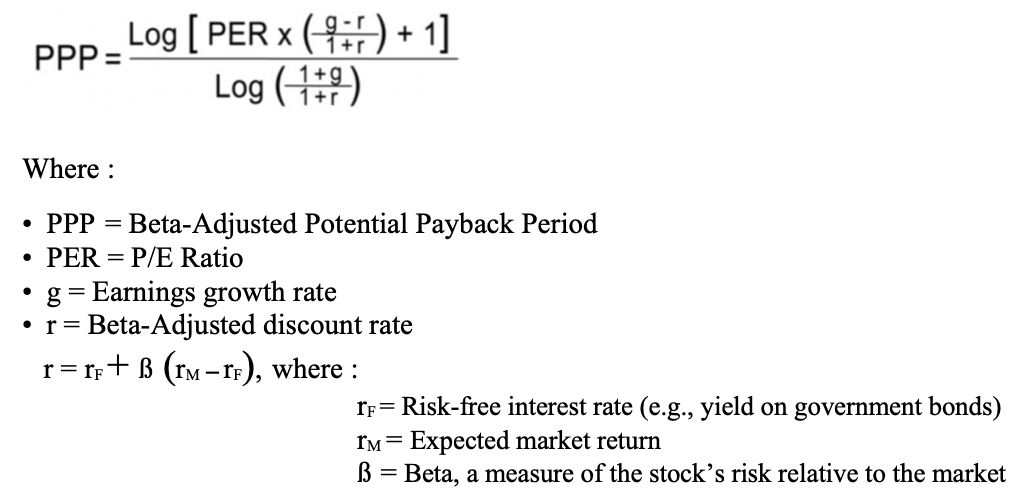

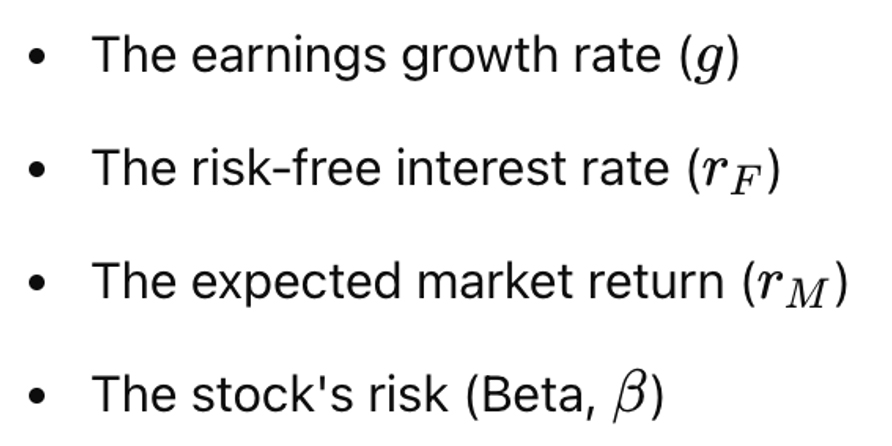

3. From PPP to SIRRIPA: Foundations of the Metric

The Potential Payback Period (PPP) and its associated return metrics—SIRR and SIRRIPA—form the core of a

dynamic valuation framework designed to address the limitations of traditional stock valuation tools. This

framework introduces time and risk explicitly into the analysis, allowing investors to determine how long it

will take for a stock’s cumulative discounted earnings to repay its purchase price, and what internal rate

of return this implies.

While the P/E ratio remains a useful starting point for assessing valuation, it is static and blind to

growth, risk, and reinvestment dynamics. In contrast, PPP generalizes the P/E by embedding these dimensions,

and SIRRIPA extends it further by expressing valuation in the form of a yield-based return metric

structurally analogous to bond Yield to Maturity (YTM).

3.1. The Logic Behind the Potential Payback Period (PPP)

The PPP answers a fundamental question in valuation:

How long does it take for an investor to recover their initial stock purchase through cumulative, discounted

earnings per share (EPS)?

The answer depends on:

• The initial P/E ratio,

• The expected earnings growth rate over time,

• The discount rate used to reflect risk and time value of money.

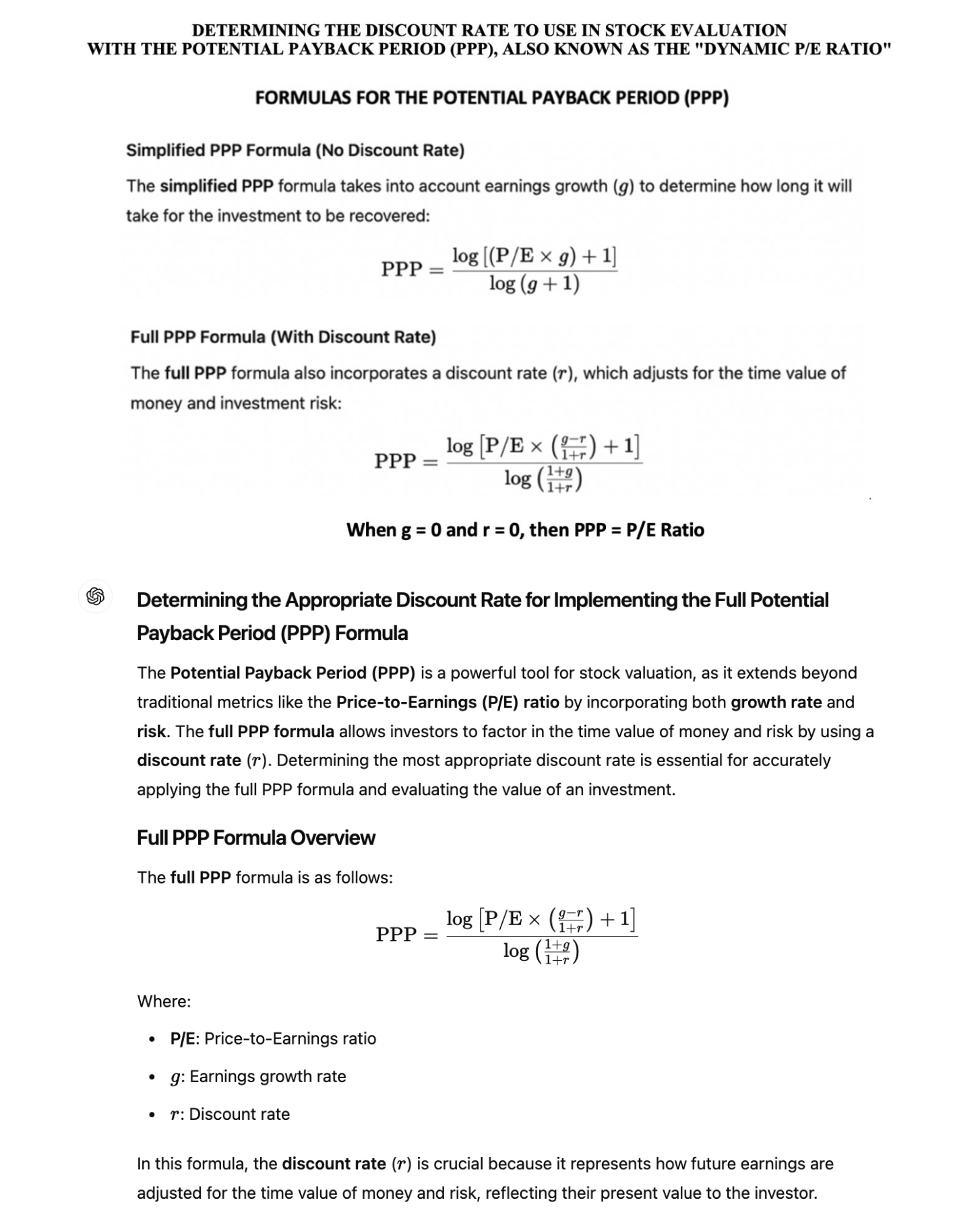

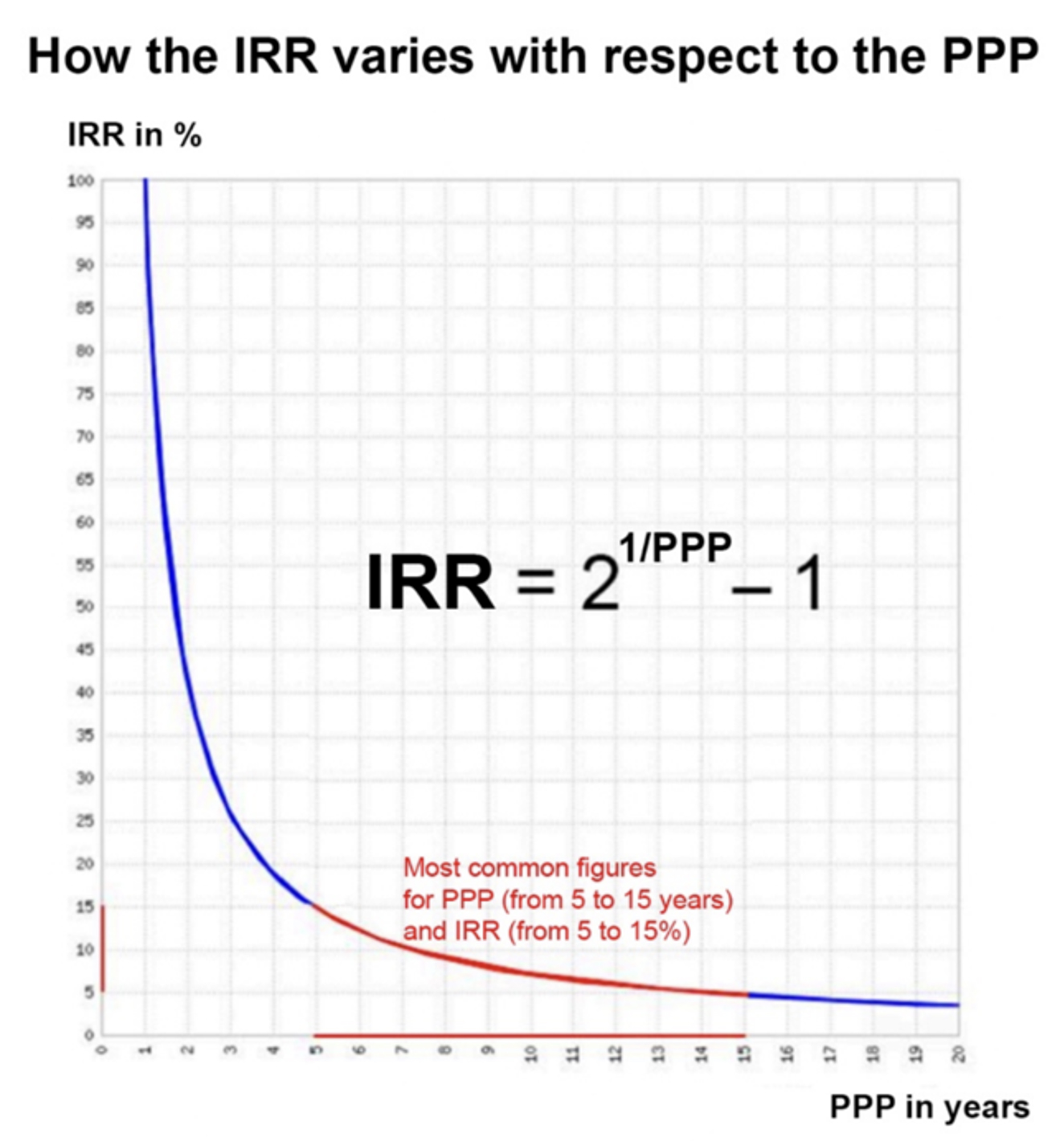

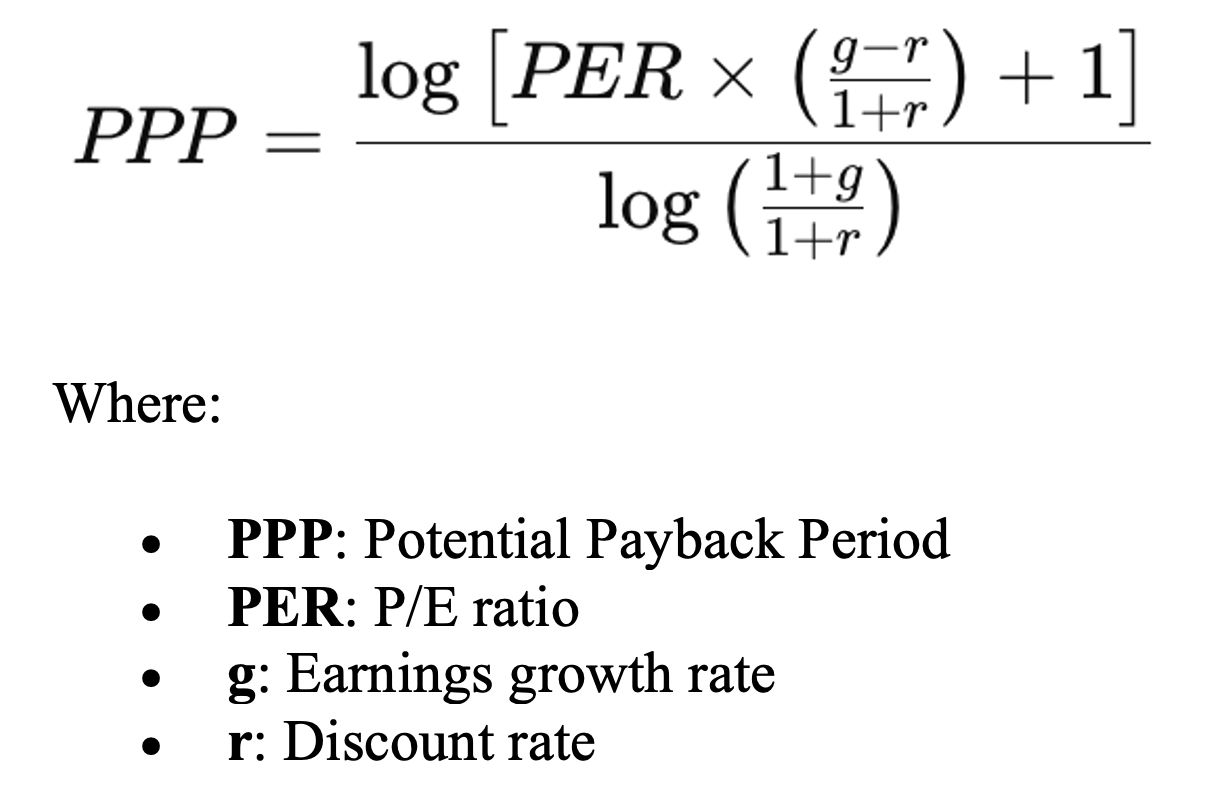

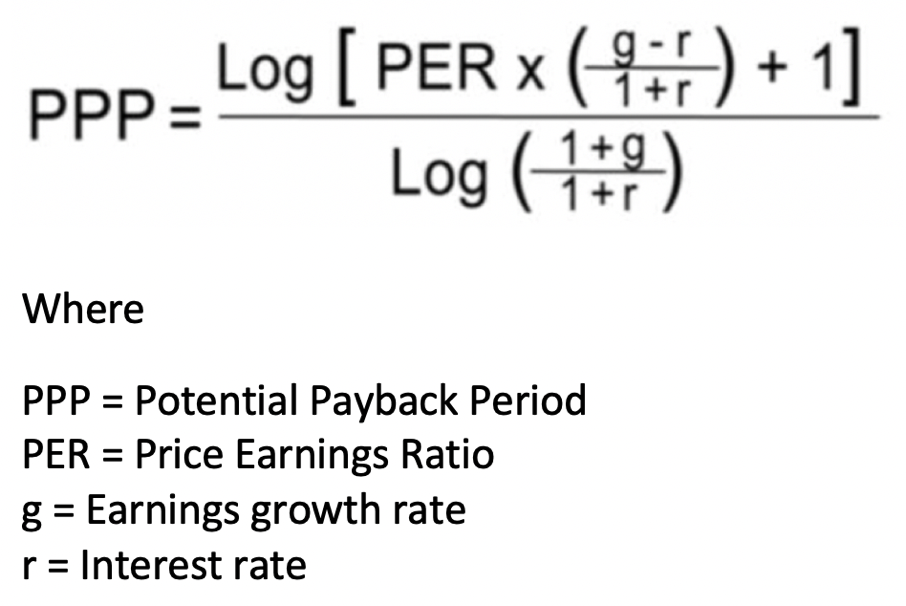

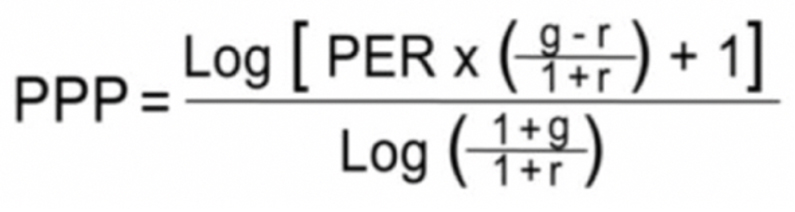

To capture these dynamics, the PPP formula is defined as:

where:

where:

• P/E is the price-to-earnings ratio,

• g is the expected initial earnings growth rate,

• r is the discount rate (typically derived from CAPM).

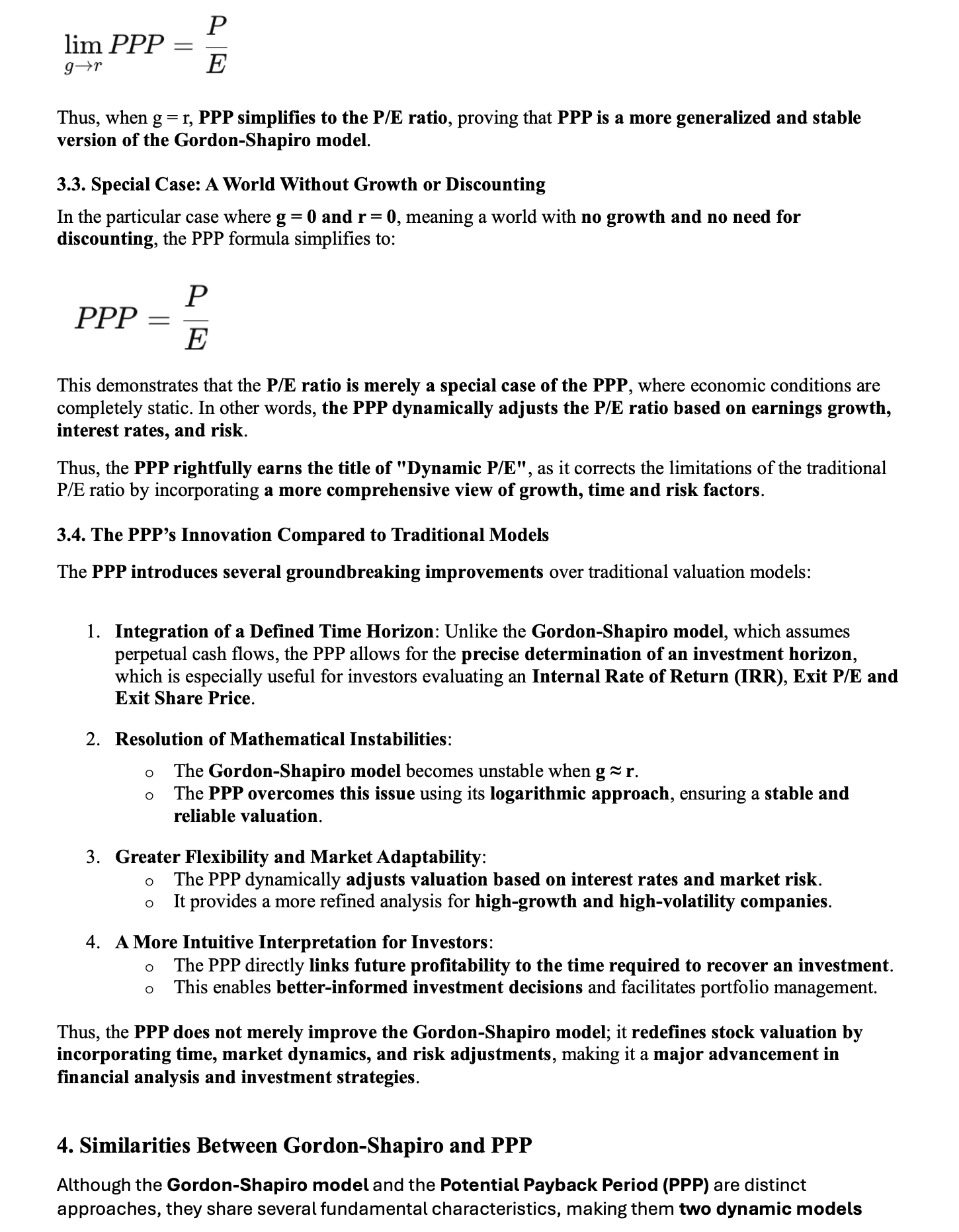

As demonstrated in [10], the P/E ratio is revealed as a special case of PPP when both g = 0 and r = 0. This

confirms that PPP is not a rejection of the P/E ratio, but its dynamic generalization, extending it into a

time- and risk-aware framework.

3.2. The Prudent Assumption of Linearly Declining Growth

A key refinement in the PPP-SIRRIPA methodology is the assumption that earnings growth declines linearly

from the initial rate g to the discount rate r over the PPP horizon. This assumption is both realistic and

prudent, and it reflects the typical trajectory of a maturing business.

Rationale for this assumption:

• Empirical realism: Most companies do not sustain high

growth indefinitely. As businesses mature,

competitive pressures, market saturation, and diminishing marginal returns reduce growth rates.

• Theoretical consistency: As shown in [3] and [4], the

linear decline from g to r ensures that the exit

valuation at the end of PPP remains grounded, reflecting the market’s tendency to value mature firms at a

P/E consistent with their risk-adjusted expected return.

• Valuation stability: By modeling earnings growth as

declining rather than constant, we avoid

overestimating terminal earnings and reduce sensitivity to extreme assumptions—common flaws in DCF and

perpetual growth models.

Under this assumption, the average growth rate ḡ over the PPP period is calculated as:

This average growth rate is used in projecting future EPS and determining the Exit Price, as detailed below.

It effectively replicates the result of earnings growing at a rate that declines linearly from g to r over

the PPP horizon.

3.3. Deriving Return Metrics from PPP

Once the PPP is known, two return metrics can be derived:

This average growth rate is used in projecting future EPS and determining the Exit Price, as detailed below.

It effectively replicates the result of earnings growing at a rate that declines linearly from g to r over

the PPP horizon.

3.3. Deriving Return Metrics from PPP

Once the PPP is known, two return metrics can be derived:

a. SIRR — Stock Internal Rate of Return (Without Exit Price)

This metric expresses the average annualized return implied by cumulative discounted earnings

alone—excluding price appreciation. It is analogous to the yield of a zero-coupon bond, where returns stem

solely from internal cash flow accumulation.

This metric expresses the average annualized return implied by cumulative discounted earnings

alone—excluding price appreciation. It is analogous to the yield of a zero-coupon bond, where returns stem

solely from internal cash flow accumulation.

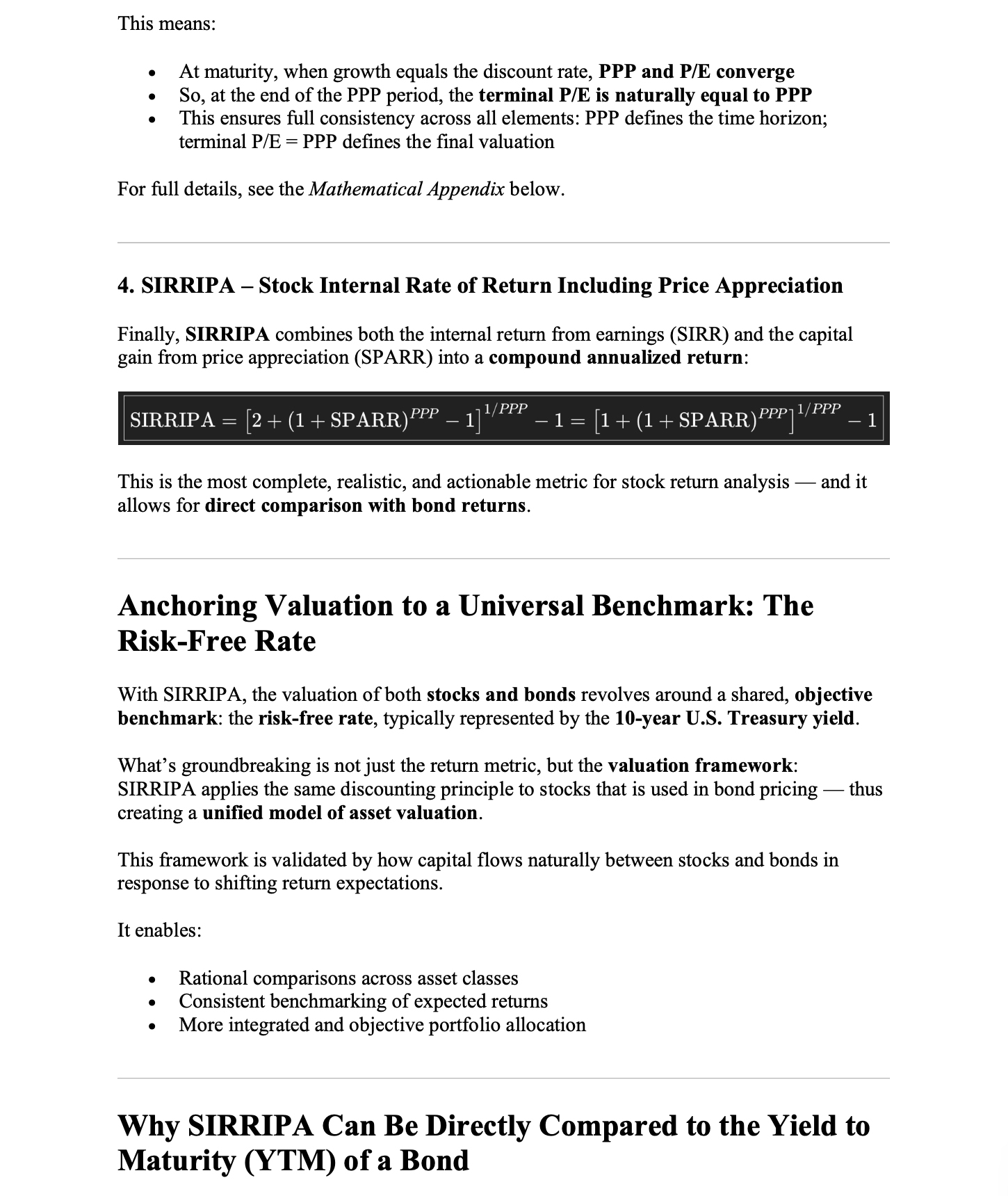

b. SIRRIPA — Stock Internal Rate of Return Including Price Appreciation

SIRRIPA builds upon SIRR by incorporating both:

• The stream of discounted EPS, and

• The Exit Price, defined at the end of the PPP horizon.

Where:

Where:

This Exit P/E formulation has two critical properties:

This Exit P/E formulation has two critical properties:

1. Mathematical Consistency: When g = r, the PPP formula simplifies—via L’Hospital’s Rule—to yield an Exit

P/E equal to PPP ⋅ (1 + r). This ensures that the valuation framework remains continuous and stable as

growth expectations converge toward the discount rate—an essential property for long-term investment

analysis.

2. Financial Realism: As a company matures, its earnings growth rate typically declines toward the market’s

required return. At that point, the appropriate P/E multiple contracts to a level consistent with the firm’s

normalized return on capital and risk profile. The fact that the Exit P/E ratio naturally contracts to the

smaller figure of PPP when "g = r" is not merely a mathematical artifact—it reflects a rational,

market-aligned valuation outcome. As shown in [4], this behavior mirrors how mature companies are priced in

practice: investors assign lower multiples as growth decelerates and risk-adjusted returns stabilize.

By tying the Exit Price to a time-sensitive, performance-based multiple rather than a speculative terminal

value, SIRRIPA reinforces the integrity of the return estimate and avoids overstatement common in

traditional models.

3.4. Relationship Between PPP, SIRR, and SIRRIPA

3.5. Replacing Arbitrary Inputs with Structured Assumptions

SIRRIPA avoids the weaknesses of conventional DCF models by:

3.5. Replacing Arbitrary Inputs with Structured Assumptions

SIRRIPA avoids the weaknesses of conventional DCF models by:

• Using a discount rate derived from CAPM, not assumed

arbitrarily,

• Establishing a natural horizon (PPP) instead of a fixed

terminal year,

• Deriving the Exit P/E from intrinsic characteristics, not

market multiples,

• Modeling growth as declining rather than perpetually

constant.

This structure removes much of the subjectivity found in traditional models and allows for valuation and

return measurement that is both theoretically rigorous and empirically grounded.

3.6. A New Standard for Return-Based Equity Valuation

SIRRIPA is not just a model—it is a reformulation of equity valuation logic. As demonstrated in [3] and [4],

it provides:

• A return metric compatible with bond YTM,

• A time-sensitive method applicable to high-growth and

loss-making firms [6],

• A foundation for unified asset allocation and

risk-adjusted portfolio design.

By generalizing the P/E ratio, embedding declining growth, and aligning with fixed-income logic, SIRRIPA

sets the stage for a coherent, modern approach to investment analysis—one capable of handling the realities

of today’s capital markets.

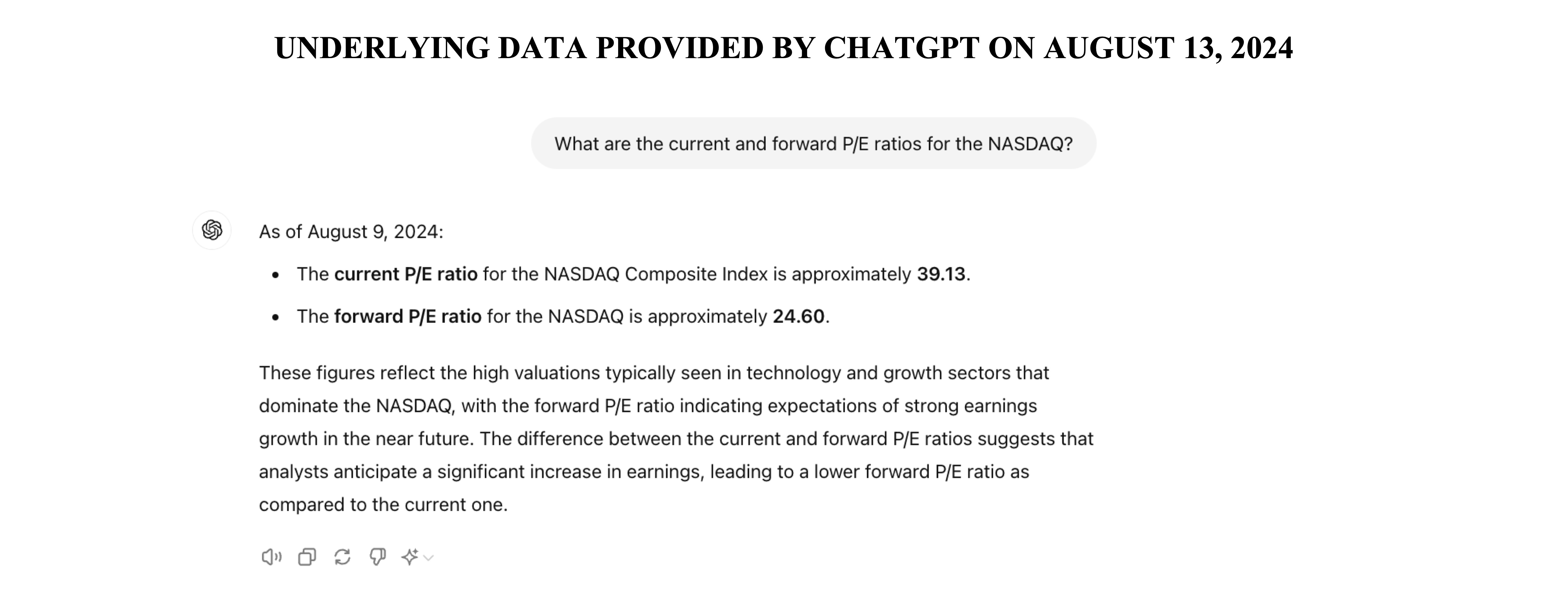

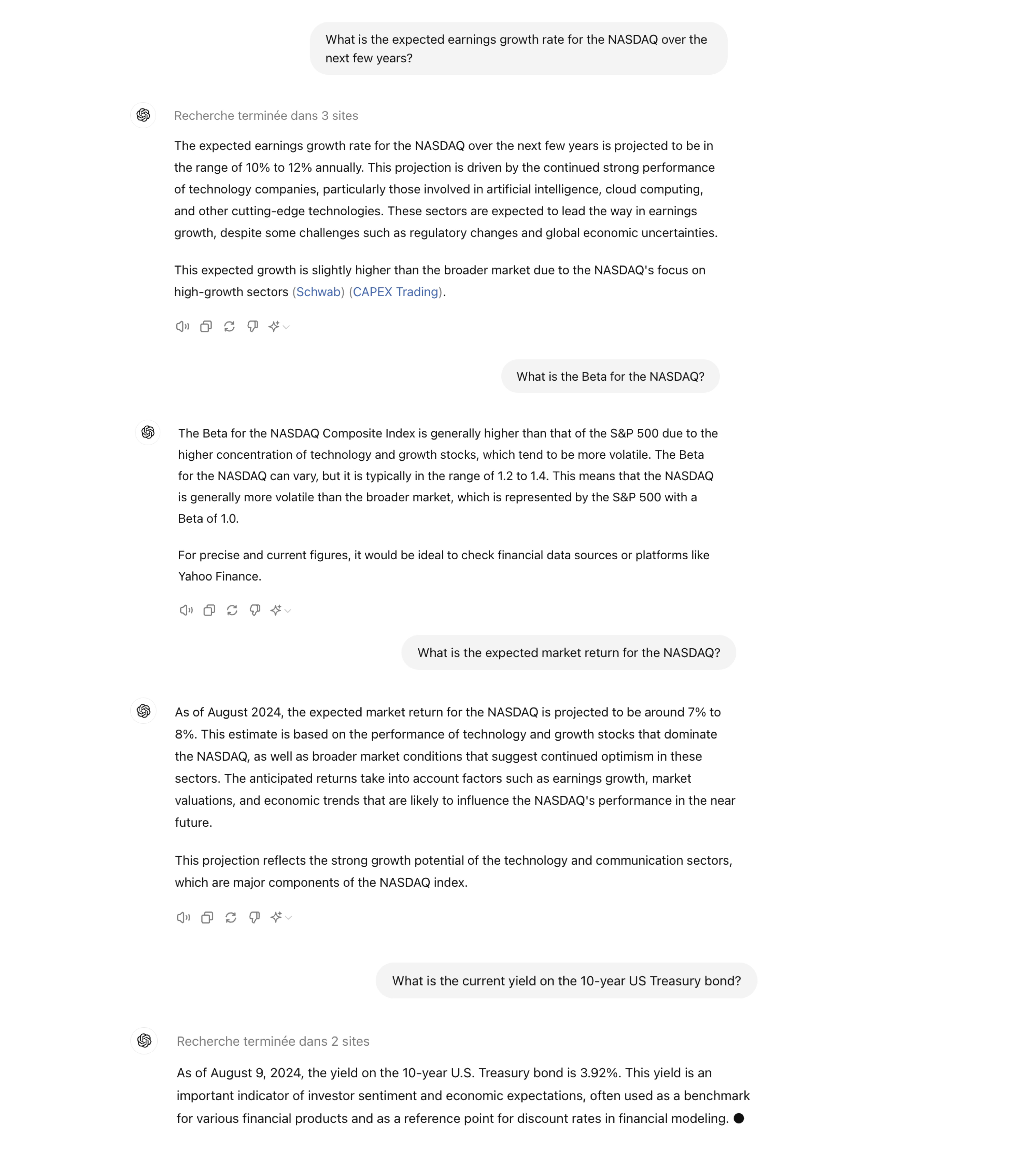

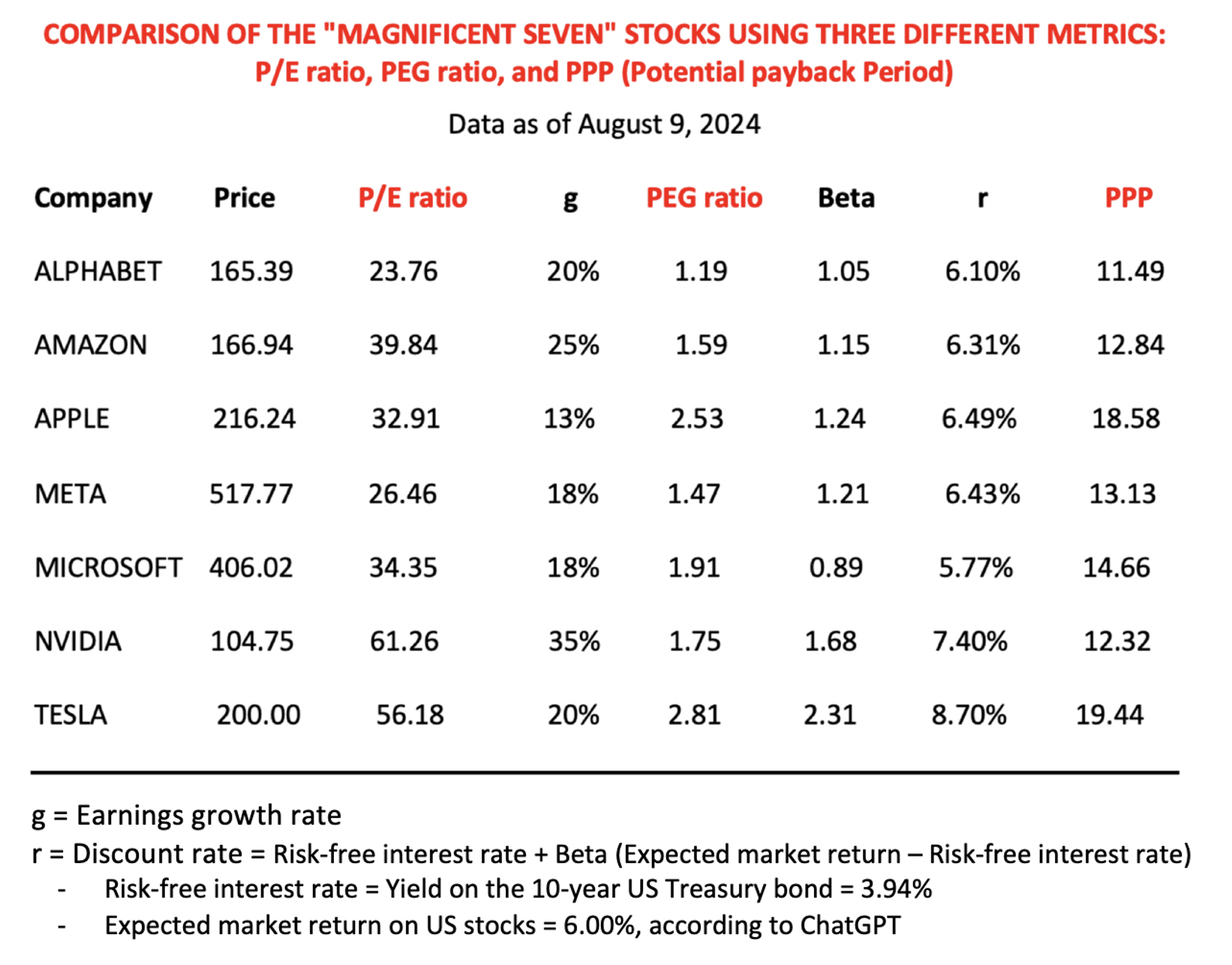

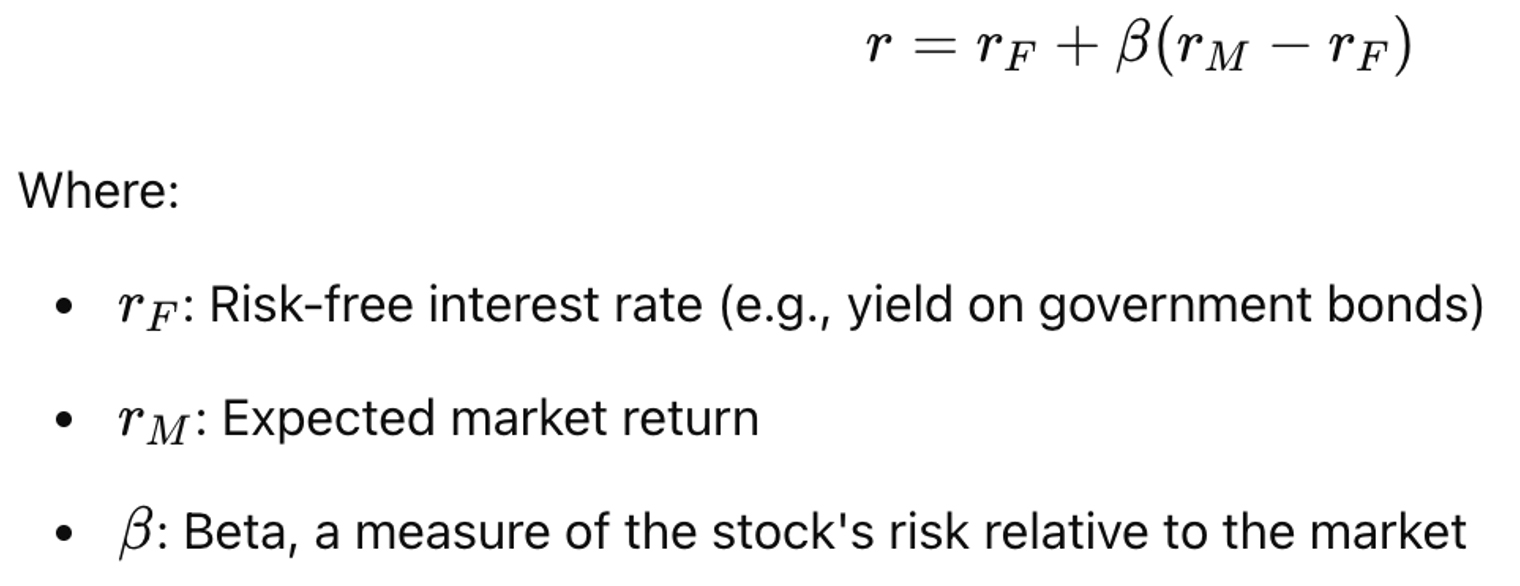

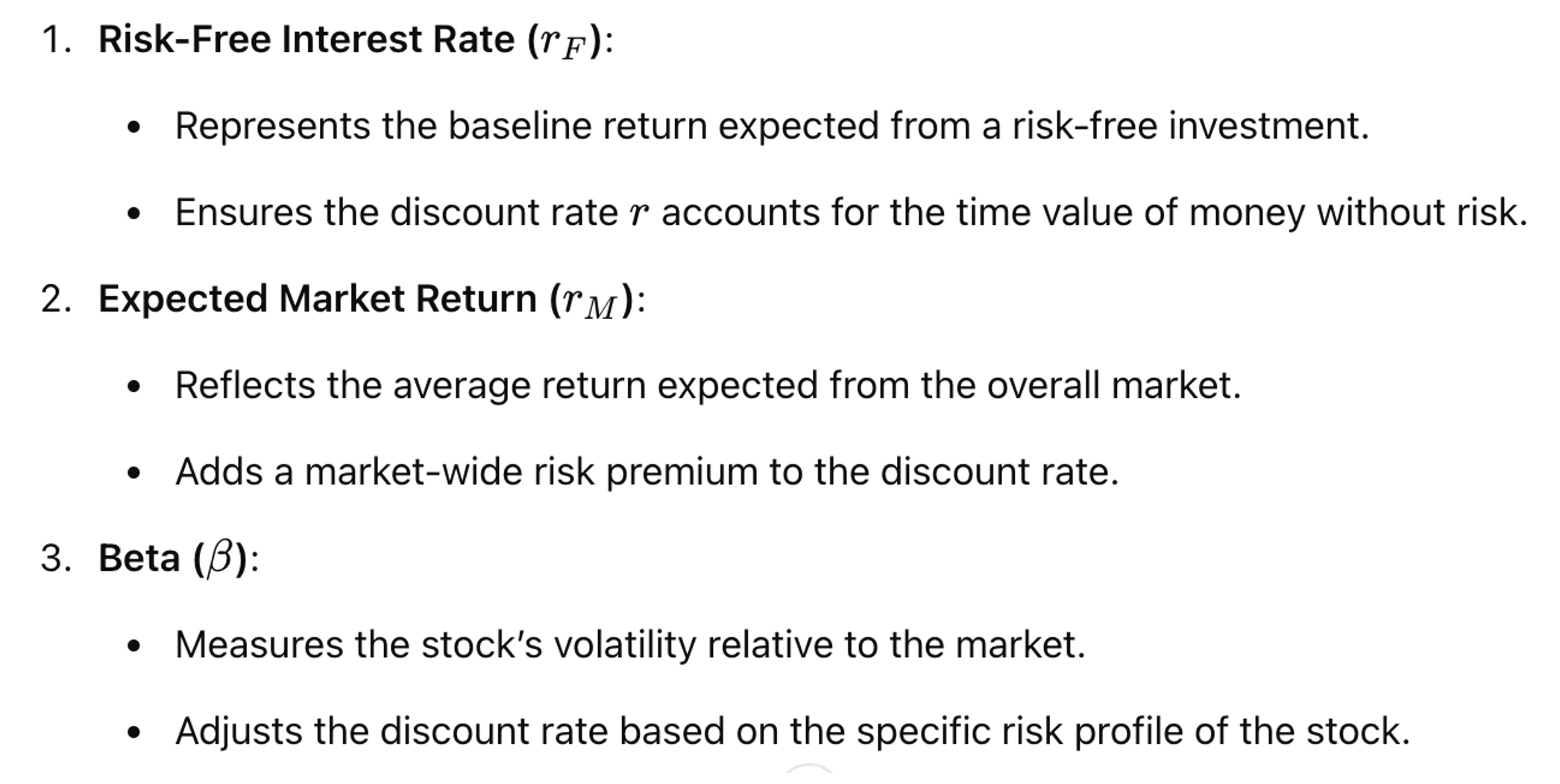

4. The Risk-Free Rate as a Common Benchmark for Bonds and Stocks

A defining innovation of the SIRRIPA framework is its alignment of equity valuation with fixed-income logic

through the shared use of the risk-free rate—typically proxied by the yield on long-term government bonds

such as the 10-year U.S. Treasury. In fixed-income markets, this rate forms the foundation for determining

the present value of future cash flows and for calculating risk premiums through yield spreads. In equity

valuation, however, traditional metrics such as the P/E ratio or PEG ratio generally operate without an

explicit benchmark, rendering risk and time largely implicit or absent altogether.

SIRRIPA resolves this inconsistency by anchoring stock valuation to the same foundational reference point as

bond valuation. By doing so, it enables both coherent risk pricing and cross-asset comparability,

establishing the risk-free rate as a universal benchmark for forward-looking return analysis.

4.1. From Bonds to Stocks: Anchoring Equity Valuation to the Risk-Free Rate

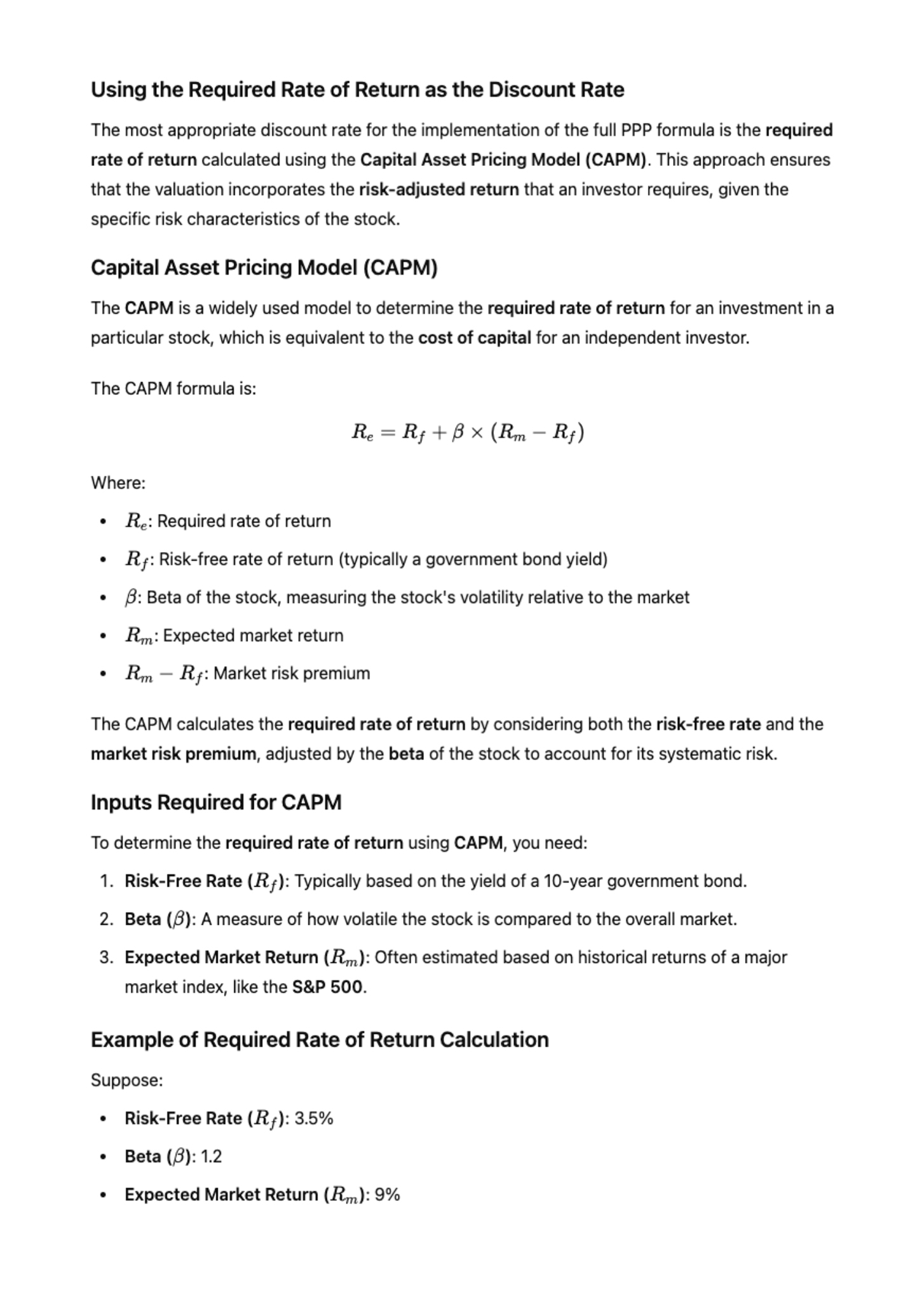

In fixed-income valuation, the Yield to Maturity (YTM) reflects the total expected return from a bond,

incorporating both periodic coupons and the final redemption value. It is calculated as the internal rate of

return that equates the bond’s current price with the present value of its future cash flows, all discounted

at a rate derived from—or at least benchmarked against—the risk-free rate:

In equity valuation using SIRRIPA, a similar structure emerges. The stock’s earnings stream (analogous to

coupons) and terminal Exit Price (analogous to face value) are discounted at a rate derived from the Capital

Asset Pricing Model (CAPM):

In equity valuation using SIRRIPA, a similar structure emerges. The stock’s earnings stream (analogous to

coupons) and terminal Exit Price (analogous to face value) are discounted at a rate derived from the Capital

Asset Pricing Model (CAPM):

Here, the discount rate r represents the minimum required return for an investor holding a given stock, and

it is explicitly anchored to the same risk-free rate rf used in fixed-income pricing. This shared foundation

enables direct comparison of returns across asset classes using structurally analogous logic.

4.2. SIRRIPA and the Risk-Free Rate: A Yield-Based Paradigm for Equities

The SIRRIPA formula calculates the internal rate of return from both earnings and terminal value, discounted

using r, which incorporates the risk-free rate rf :

Here, the discount rate r represents the minimum required return for an investor holding a given stock, and

it is explicitly anchored to the same risk-free rate rf used in fixed-income pricing. This shared foundation

enables direct comparison of returns across asset classes using structurally analogous logic.

4.2. SIRRIPA and the Risk-Free Rate: A Yield-Based Paradigm for Equities

The SIRRIPA formula calculates the internal rate of return from both earnings and terminal value, discounted

using r, which incorporates the risk-free rate rf :

This formulation makes the risk-free rate rf an integral part of the valuation framework:

This formulation makes the risk-free rate rf an integral part of the valuation framework:

• It defines the discount rate r through CAPM,

• It shapes the Exit P/E multiple, via Exit P/E = PPP ⋅ (1 +

r),

• It enables the extraction of the equity risk premium as:

Stock Risk Premium (SRP) = SIRRIPA − rf

This last point is particularly significant. Just as the credit spread in bonds quantifies the market’s

pricing of risk over the risk-free baseline, the SRP measures the forward-looking compensation equity

investors require—not based on historical returns, but derived structurally from valuation inputs and cash

flow expectations.

4.3. Why This Alignment Is Transformative

Aligning equity valuation with bond methodology through a shared benchmark yields several powerful

advantages:

4.3.1. Unified Return Language Across Asset Classes

SIRRIPA makes it possible to compare a stock with a SIRRIPA of 10.2% and a bond with a YTM of 7.5%, both

measured against the same risk-free rate rf . This supports rational asset allocation, capital budgeting,

and performance benchmarking on a consistent basis.

4.3.2. Transparent and Dynamic Risk Pricing

Traditional valuation methods obscure risk by omitting explicit benchmarks. SIRRIPA formalizes the discount

rate using observable market inputs (risk-free rate and equity risk premium), which update dynamically with

economic conditions and investor sentiment.

4.3.3. Elimination of Arbitrary Discounting

In many DCF implementations, the discount rate is chosen arbitrarily—often defaulting to a static “rule of

thumb” (e.g., 10%). SIRRIPA replaces this with a theoretically grounded, CAPM-derived rate tied directly to

the prevailing interest rate environment.

4.3.4. Cross-Asset Optimization and Risk Budgeting

Institutional investors often struggle to balance equity and fixed-income allocations due to incompatible

return metrics. SIRRIPA enables apples-to-apples comparison, enhancing portfolio construction, risk parity

models, and stress-testing scenarios.

4.4. Empirical and Theoretical Reinforcement

This alignment of discounting logic and benchmark consistency has been validated in several of our prior

works:

• In [12], we demonstrate how using CAPM-derived discount

rates improves the interpretability and

comparability of DCF-based valuations under the SIRRIPA framework.

• In [3], SIRRIPA is shown to provide a bond-like return

metric for equities, allowing for real-time

comparison between growth stocks and yield-oriented instruments.

• In [17], we show how replacing the fixed assumptions of

the Gordon-Shapiro Model with time-sensitive,

risk-adjusted logic centered around the risk-free rate significantly improves valuation precision.

Collectively, these studies reinforce that anchoring SIRRIPA to the risk-free rate is not merely a

structural choice—it is a conceptual advancement that brings equity valuation into alignment with the

broader logic of capital markets.

4.5. A Common Valuation Standard for a Unified Capital Market

As capital markets become more integrated and asset allocators demand more consistent, transparent

frameworks, the use of the risk-free rate as a common anchor across asset classes becomes a baseline

requirement, not an analytical luxury.

The SIRRIPA framework meets this requirement by:

• Bridging fixed-income and equity valuation through

shared assumptions,

• Offering a risk-aware, time-dependent return

metric, and

• Supporting macro-consistent policy, regulatory, and

portfolio-level modeling.

In doing so, SIRRIPA does not simply reform equity valuation; it harmonizes it with the broader structure of

return-based decision-making across the financial system.

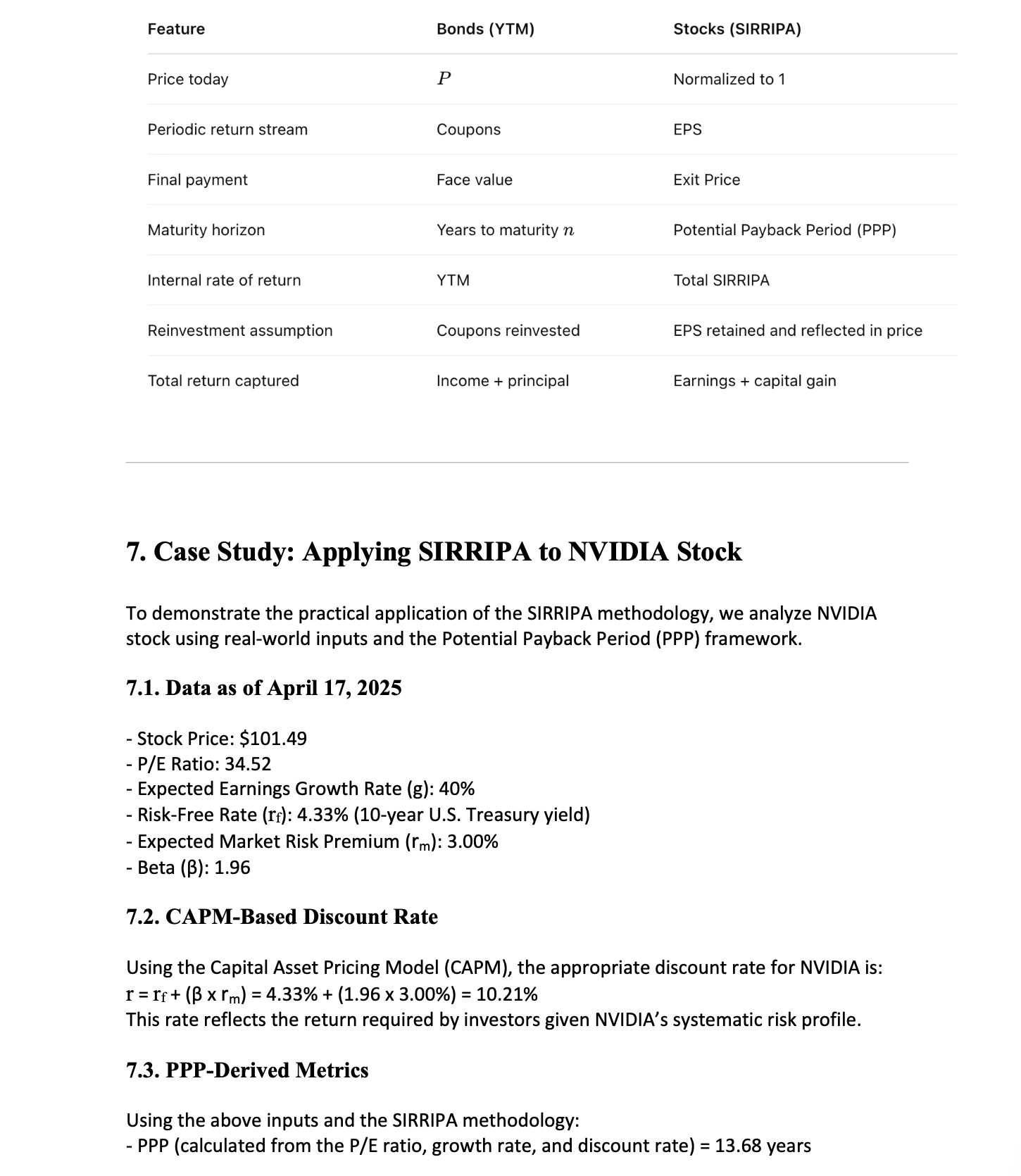

5. Comparing the Components of Return: Stocks vs. Bonds

A critical breakthrough enabled by the SIRRIPA framework is the recognition that the return structures of

stocks and bonds—while superficially different—are economically and mathematically comparable when viewed

through the proper conceptual lens. This section explains two essential equivalences that form the

foundation of this comparability, supported by real-world examples and rigorous financial theory.

5.1. Why Earnings per Share (EPS) Are Analogous to Bond Coupons

In bond valuation, coupon payments represent fixed, periodic cash flows contractually promised to

bondholders. These coupons form the backbone of a bond’s Yield to Maturity (YTM)—a return measure that

incorporates all future cash flows discounted to the present.

In equity valuation, the equivalent flow is not the dividend, but the Earnings Per Share (EPS). While

dividends represent the portion of earnings distributed, EPS captures the full economic value generated on

behalf of shareholders, including amounts retained by the company for reinvestment and future growth.

This leads to a fundamental equivalence:

EPS functions as the equity analog of bond coupons, because both represent recurring, value-generating flows

that belong to the investor—whether paid out or retained.

Supporting Rationale:

• Economic Equivalence: Rational investors are indifferent between receiving earnings via dividends

or

through retained reinvestment, provided that reinvested earnings yield adequate returns (per the

Modigliani–Miller theorem).

• Discounted Cash Flow Logic: In SIRRIPA, projected EPS are discounted over the Potential Payback

Period

(PPP), just as bond coupons are discounted over a bond’s life to compute YTM.

• Growth and Reinvestment: EPS inherently includes future value creation via compounding, similar to

bonds

with reinvested coupons.

This conceptual alignment is illustrated in [15], "NVIDIA Leads in Forward Returns", where stocks

with

modest dividend policies—but strong EPS growth—generate high SIRRIPA values. The analogy holds: reinvested

EPS in stocks acts like reinvested interest in bonds. The theoretical foundation for this treatment is

elaborated in [9], "Mathematics of Stock Valuation", and is consistent with frameworks found in [19]

Damodaran, [20] Penman, and [21] Koller et al.

5.2. Why Exit Price Is Analogous to a Bond’s Face Value or Redemption Price

In fixed-income investing, the face value (or redemption price) is the terminal payment a bondholder

receives at maturity. In calculating YTM, this lump sum is discounted along with the coupons to compute a

bond’s total return.

In equity valuation under the SIRRIPA framework, a parallel concept exists: the Exit Price. It reflects the

market value of the stock at the end of the PPP period and is calculated as:

This approach ensures that the Exit Price:

This approach ensures that the Exit Price:

• Avoids speculation, by anchoring the terminal multiple to a function of time and risk.

• Incorporates growth, via the projected EPS at the end of PPP.

• Plays the same role as bond principal, by representing a final, discounted value that adds to the

total

return.

This analogy is applied in [14], "Resolving the Valuation Mystery of Palantir Technologies", where an

extreme forward P/E is rationalized through long-term earnings growth and a realistic Exit P/E. Despite a

current P/E above 500, the SIRRIPA calculation shows how long-term earnings and prudent exit valuation

produce a justifiable return—just as a zero-coupon bond trading at a steep discount can deliver competitive

YTM.

Similarly, [16], "The Insolent, Persistent Bull Market on Wall Street", demonstrates how upward momentum in

stock prices can be explained by retained earnings compounding over time, not short-term multiples—analogous

to premium bonds appreciating toward face value at maturity.

5.3. Summary Table: Structural Comparison Between Bonds and Stocks under SIRRIPA

5.4. Implication: Structural Equivalence Unlocks Rational Comparability

The above equivalences are not just theoretical—they are transformative. SIRRIPA re-engineers equity

valuation into a format that mirrors fixed-income logic, making it possible to:

5.4. Implication: Structural Equivalence Unlocks Rational Comparability

The above equivalences are not just theoretical—they are transformative. SIRRIPA re-engineers equity

valuation into a format that mirrors fixed-income logic, making it possible to:

• Compare stocks to bonds on a common risk-adjusted, time-sensitive basis.

• Value retained earnings and price appreciation without speculative projections.

• Incorporate market-based benchmarks such as the risk-free rate and CAPM-based discounting.

• Rationalize "irrational" market valuations by recasting them as time-based earnings realizations.

This structural equivalence also aligns with traditional and modern valuation thought. As demonstrated in

[22] Graham and Dodd’s Security Analysis and extended in [23] Value Investing: From Graham to Buffett and

Beyond, sound valuation always rests on linking price to long-term economic fundamentals—precisely what

SIRRIPA does by synthesizing periodic earnings and final price into one yield-like metric.

In doing so, SIRRIPA doesn’t just measure return—it unifies equity and bond valuation into a coherent,

comparable, and risk-sensitive system.

6. Implications for Investment, Policy, and Analysis

The emergence of SIRRIPA as a yield-based valuation metric for equities—structurally and mathematically

analogous to Yield to Maturity (YTM) in bonds—represents more than a methodological advance. It marks a

paradigm shift with wide-ranging consequences for portfolio construction, valuation theory, regulatory

modeling, and cross-asset capital allocation.

By establishing a time-sensitive, risk-adjusted, and internally consistent return framework rooted in the

Potential Payback Period (PPP), SIRRIPA offers a clear and unified lens through which modern equity

investments can be evaluated. This section explores the implications of this shift across three interrelated

domains: investors, analysts and academics, and public policy.

6.1. For Investors and Asset Managers: A Bond-Like Lens for Equity Portfolios

In institutional and retail investment strategy, the ability to compare expected returns across asset

classes is central to portfolio optimization. Bonds are evaluated using forward-looking yield metrics (e.g.,

YTM, effective duration), while equities are typically assessed using static or partial indicators (e.g.,

P/E ratios, dividend yield, growth forecasts).

SIRRIPA addresses this asymmetry by:

• Delivering a comprehensive annualized return metric for equities,

• Incorporating earnings trajectory, capital appreciation, and risk discounting,

• Enabling direct comparison with bond yields, mortgage-backed security IRRs, and even real estate cap

rates.

This equips asset managers to:

• Construct more coherent multi-asset portfolios,

• Match liabilities and forecast cash flows more precisely,

• Allocate capital based on time-adjusted risk premiums.

As illustrated in [3] and [4], applying SIRRIPA to stocks enables apples-to-apples comparison with

fixed-income products, helping to identify mispriced securities or strategic tilts based on the evolving

macroeconomic landscape (e.g., interest rate normalization, inflation cycles, or yield curve shifts).

6.2. For Analysts and Academics: A Return Metric That Restores Internal Consistency

In financial theory, valuation models are often based on discounted cash flows, yet the practice of equity

analysis is frequently dominated by ratios that fragment value (P/E, PEG, EV/EBITDA). This creates a

disconnect between theoretical rigor and applied metrics.

SIRRIPA resolves this inconsistency by:

• Synthesizing time, growth, and risk into one metric,

• Retaining the logic of present value modeling while avoiding speculative assumptions,

• Extending foundational valuation frameworks like the Gordon Growth Model (GGM) with finite-horizon realism

[17, 18].

From a pedagogical standpoint, SIRRIPA offers a powerful teaching tool:

• It bridges the gap between bond math and equity modeling,

• It reorients valuation around recovery time and yield, not just valuation multiples,

• It introduces a stock-specific internal rate of return, analogous to IRR in project finance and private

equity.

For empirical researchers, SIRRIPA offers a more robust measure for backtesting investment strategies,

modeling cross-sectional returns, or building factor-based models that integrate forward-looking valuation

with time sensitivity.

6.3. For Policymakers and Regulators: A Step Toward Unified Financial Standards

The financial system depends on consistent frameworks for evaluating risk and return. Regulators require

asset managers, insurers, and pension funds to model solvency and funding status across economic scenarios.

Yet, they still face fundamental inconsistencies:

• Bonds and stocks are modeled using incompatible valuation frameworks,

• Discount rate assumptions vary widely across sectors and institutions,

• Risk premiums are often estimated ex post, rather than derived structurally.

SIRRIPA addresses these challenges by:

• Offering a standardized, forward-looking return measure for equities that is anchored to the risk-free

rate,

• Providing a tool for stress-testing portfolios under interest rate or earnings growth scenarios,

• Supporting cross-asset risk calibration for policy models (e.g., capital adequacy, ALM models, solvency

frameworks).

For sovereign wealth funds, pension boards, and financial stability councils, SIRRIPA can serve as a

framework for risk-adjusted performance benchmarking, helping institutions assess whether expected returns

are aligned with funding requirements, risk constraints, and macroeconomic conditions.

6.4. Strategic and Practical Integration

Adopting SIRRIPA need not require discarding all legacy valuation methods. Rather, it can be integrated into

existing analysis as a synthesis metric:

• Use alongside DCF models to validate assumptions about capital recovery,

• Compare with P/E or PEG to detect when traditional ratios fail to account for growth timing or risk,

• Overlay with factor models or equity screens to identify misaligned valuation-risk profiles.

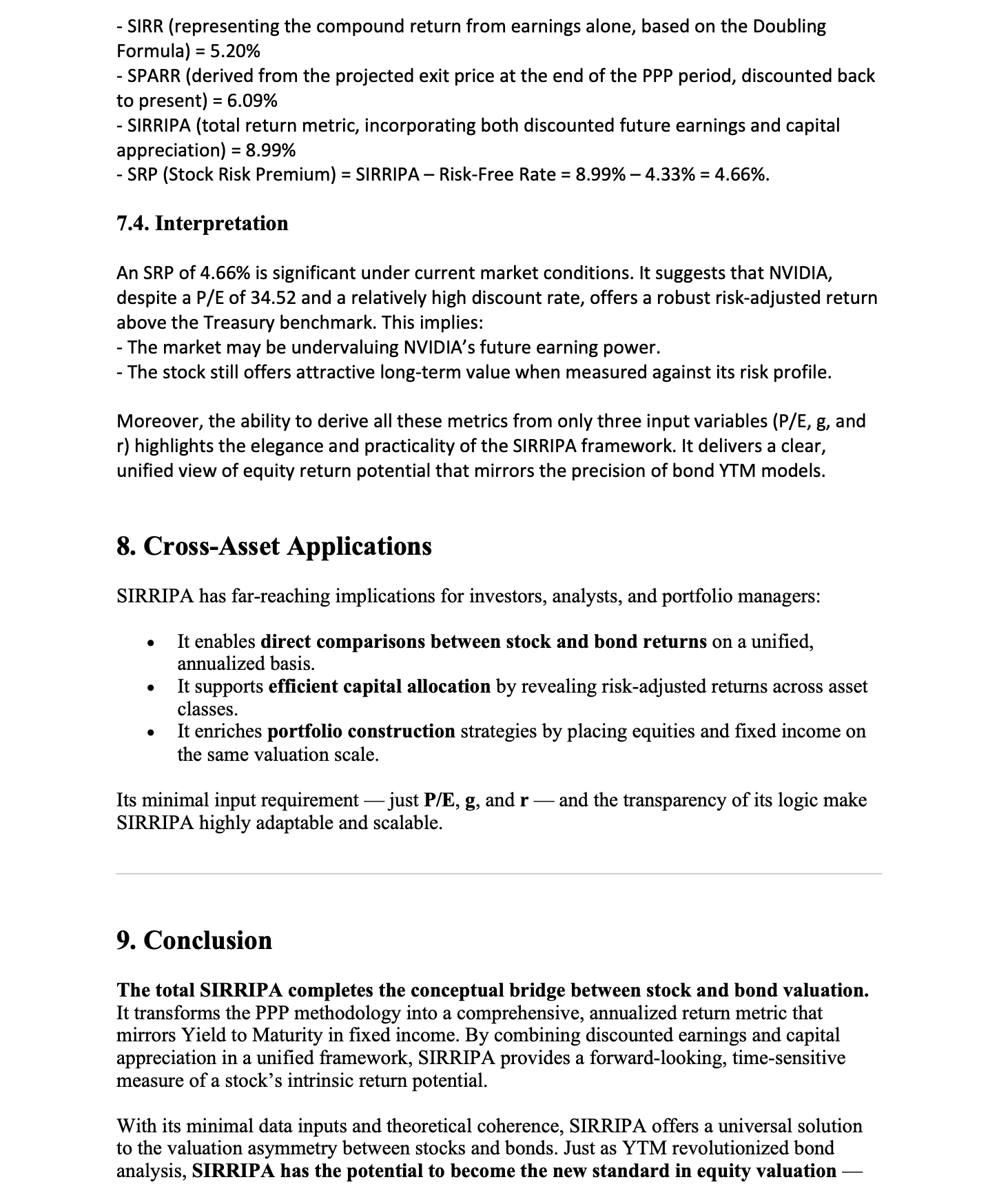

As shown across applications in [13], [14], [15], and [16], SIRRIPA is especially valuable for analyzing:

• High-growth or speculative stocks with extreme P/E ratios,

• Loss-making firms that are difficult to evaluate using static ratios [6],

• Interest-sensitive equities in a changing rate environment.

In this way, SIRRIPA becomes not just a new metric, but a core pillar of a valuation system—unifying the

precision of bond analysis with the growth dynamics of equity investment.

7. Conclusion: From Static Multiples to Dynamic Metrics

The dominant tools of traditional equity valuation—such as the P/E ratio, PEG ratio, Dividend Yield, and

even the Gordon-Shapiro Model—have served generations of investors and analysts. They are accessible,

intuitive, and deeply embedded in financial practice. Yet they are also products of a simpler analytical

era—one less attuned to the complexities of reinvestment, variable growth trajectories, cross-asset

allocation, and risk-adjusted return modeling.

At their core, these tools share fundamental structural limitations:

• They are static or one-dimensional, failing to capture the evolution of earnings over time.

• They are incomplete, often separating income from capital gains or focusing solely on distributions.

• They are incompatible with fixed-income valuation frameworks, preventing unified analysis across bonds and

equities.

The SIRRIPA framework—grounded in the Potential Payback Period (PPP)—addresses these deficiencies by

integrating the four essential dimensions of valuation: earnings, growth, risk, and time. It synthesizes

them into a single, yield-based return metric that allows equities to be evaluated in the same logic and

language long reserved for bonds:

• Just as Yield to Maturity (YTM) reflects both periodic coupons and terminal repayment,

• SIRRIPA integrates cumulative discounted earnings and a rational, performance-based Exit Price.

This alignment is more than a mathematical innovation—it represents a conceptual convergence. It places

equity valuation on equal footing with fixed-income analysis, providing a time-aware, risk-adjusted

framework for return forecasting, asset comparison, and capital allocation.

By treating Earnings Per Share (EPS) as the equity analogue of bond coupons and the Exit Price as analogous

to a bond’s face value, SIRRIPA offers a practical, internally consistent answer to the most fundamental

investment questions:

How much will I earn? Over what time? At what risk? Compared to what?

Because the framework is built on first principles—mathematically sound and adaptable to modern financial

modeling—it has the potential to integrate seamlessly into academic theory, practitioner toolkits,

regulatory guidelines, and fintech platforms.

In a financial world increasingly focused on comparability, transparency, and precision, SIRRIPA is not

merely an enhancement of legacy metrics. It redefines how value is measured—moving from static multiples to

dynamic, time-based return metrics—and lays the groundwork for a unified valuation methodology across the

full spectrum of investable assets.

That said, it is important to recognize the limitations and evolving nature of this approach. As a return

metric designed to evaluate a stock’s attractiveness on the same basis as a bond—anchored to the risk-free

rate as a universal benchmark—SIRRIPA may understandably challenge conventional valuation norms. While not

without its limitations, and subject to reasonable debate concerning its assumptions and computational

structure, the framework presented here aims to demonstrate its coherence and relevance as a forward-looking

tool for valuation.

The PPP and its derivative metrics are relatively new, and there is a pressing need for continued

research—both conceptual and empirical—to refine their theoretical foundations, test their predictive

validity, and assess their applicability across a wide range of industries, market cycles, and geographies.

Moreover, like all financial models, the reliability of PPP-based valuation is constrained by the quality of

its inputs—most notably projected earnings growth rates, discount rates, and risk measures such as beta.

Even the most rigorous framework can yield misleading results if built on flawed or overly optimistic

assumptions. This underscores the critical importance of sensitivity analysis, which must accompany any

serious valuation exercise using PPP or its derivatives to assess the robustness of conclusions under

varying input scenarios.

Ultimately, no model can capture every relevant variable or anticipate all market dynamics. The objective is

not to predict the future with certainty, but to reflect economic reality as faithfully as possible—while

offering a logically consistent, transparent, and decision-relevant approach to valuation. In this respect,

SIRRIPA represents both a theoretical advance and a practical tool—one that encourages more disciplined

thinking about return, risk, and time in modern equity markets.

References I- Articles Introducing or Applying the PPP and SIRRIPA Framework [1] Sam, R. (1984). Le P.E.R., un instrument mal adapté à la gestion mondiale des portefeuilles. Comment remédier à ses lacunes. Analyse Financière. https://www.stockinternalrateofreturn.com/Analyse-Financie%CC%80re_1.pdf [2] Sam, R. (2023). Stock Evaluation: Discovering the Potential Payback Period (PPP) as a Dynamic P/E Ratio. Website. https://www.stockinternalrateofreturn.com/index.html [3] Sam, R. (2025). SIRRIPA: The Stock-Tailored Yield to Maturity (YTM) and the Emergence of a Cross-Asset Valuation Metric. https://doi.org/10.20944/preprints202504.1934.v1 [4] Sam, R. (2025). Why SIRRIPA is Set to Replace the P/E Ratio in Modern Equity Valuation. https://www.preprints.org/manuscript/202504.1213/v1 [5] Sam, R. (2025). Mathematics of Stock Valuation: Why the Potential Payback Period (PPP) Outperforms the P/E and PEG Ratios. 10.5281/zenodo.15668147 [6] Sam, R. (2025). Breaking the Valuation Deadlock: Replacing the P/E Ratio with the Potential Payback Period (PPP) for Loss-Making Companies – A Case Study on Intel (2025). http://dx.doi.org/10.2139/ssrn.5247858 [7] Sam, R. (2025). Proving that the P/E Ratio is Just a Limiting Case of the Potential Payback Period (PPP) When Earnings Growth and Interest Rate are Ignored. https://ssrn.com/abstract=5254723 [8] Sam, R. (2025). Beyond Valuation: The Four PPP-Derived Return Metrics and Their Role in Modern Equity Analysis. 0.5281/zenodo.16155541 [9] Sam, R. (2025). Mathematics of Stock Valuation: How the Potential Payback Period (PPP) Subsumes the P/E and PEG Ratios. http://dx.doi.org/10.2139/ssrn.5314340 [10] Sam, R. (2025). A Quantitative Revelation in Equity Valuation: The P/E Ratio as a Degenerate Case of the Potential Payback Period (PPP). DOI: https://doi.org/10.20944/preprints202505.2166.v1 [11] Sam, R. (2025). How to Adjust the P/E Ratio for Earnings Growth in Equity Valuation: PEG or PPP? DOI: https://doi.org/10.20944/preprints202505.0212.v1 II- Articles Addressing Specific Valuation Models (Including Gordon-Shapiro) or Case Studies [12] Sam, R. (2025). Reassessing the Discounted Cash Flow Model (DCFM): How the Potential Payback Period (PPP) Improves Applicability and Accuracy with a Time-Based Approach. http://dx.doi.org/10.2139/ssrn.5279126 [13] Sam, R. (2025). Is the S&P 500 Overvalued? All Metrics Say Yes, Except SIRRIPA. http://dx.doi.org/10.2139/ssrn.5320663 [14] Sam, R. (2025). Resolving the Valuation Mystery of Palantir Technologies: How PPP and SIRRIPA Rationalize a Market Darling with a P/E Over 500. http://dx.doi.org/10.2139/ssrn.5338179 [15] Sam, R. (2025). NVIDIA Leads in Forward Returns: A PPP-Based Stock Valuation Analysis of Four Leading Technology Firms. http://dx.doi.org/10.2139/ssrn.5337514 [16] Sam, R. (2025). The Insolent, Persistent Bull Market on Wall Street: A Rebuttal to Traditional Metrics—P/E Ratio, PEG Ratio, and Earnings Yield—and a Validation of SIRRIPA. http://dx.doi.org/10.2139/ssrn.5347721 [17] Sam, R. (2025). Revisiting the Gordon-Shapiro Model: How the Potential Payback Period (PPP) Refines and Operationalizes a Foundational Framework in Stock Valuation. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5257245 [18] Sam, R. (2025). Making the P/E Ratio a Truly Dynamic Valuation Metric: Gordon-Shapiro vs. Potential Payback Period (PPP). https://zenodo.org/records/15832809 III- Foundational and Independent Books on Valuation Theory [19] Damodaran, A. (2012). Investment Valuation: Tools and Techniques for Determining the Value of Any Asset (3rd ed.). Wiley. [20] Penman, S. H. (2013). Financial Statement Analysis and Security Valuation (5th ed.). McGraw-Hill Education. [21] Koller, T., Goedhart, M., & Wessels, D. (2020). Valuation: Measuring and Managing the Value of Companies (7th ed.). Wiley. [22] Graham, B., & Dodd, D. L. (2009). Security Analysis: Sixth Edition, Foreword by Warren Buffett. McGraw-Hill Education. [23] Greenwald, B., Kahn, J., Sonkin, P. D., & van Biema, M. (2004). Value Investing: From Graham to Buffett and Beyond. Wiley.

THE FIRST TO SEE THE WALL STREET CRASH COMING: RAINSY SAM AND THE PREDICTIVE POWER OF THE POTENTIAL PAYBACK PERIOD (PPP) Rainsy Sam — a Cambodian-born economist, equity research analyst, investment manager, and former Finance Minister — was the first to publicly predict the current Wall Street crash, which has been triggered by President Donald Trump’s chaotic economic policies. His March 12 article, “Anatomy of a Looming Bear Market: How to Assess the Impact of Donald Trump's Chaotic Economic Measures on Wall Street,” was first posted on LinkedIn, later published in the Revue Française d’Économie et de Gestion https://www.revuefreg.fr/index.php/home/article/view/2057/1636, and quickly gained traction across professional and financial networks. What distinguishes this analysis is its use of the Potential Payback Period (PPP) — a groundbreaking valuation tool that goes far beyond conventional metrics such as the P/E and PEG ratios. By integrating earnings growth, interest rates, and risk, the PPP offers a more rigorous, dynamic, and forward-looking understanding of stock market valuation. Importantly, Rainsy Sam’s prediction was not based on vague notions of “market sentiment” or subjective, non-quantified interpretations common in financial literature. Instead, it was built on explicit, quantified hypotheses about future earnings growth, supported by sensitivity analysis that demonstrated how variations in key inputs would affect the PPP, the SIRRIPA (Stock Internal Rate of Return Including Price Appreciation), and ultimately, the SRP (Stock Risk Premium) representing the difference between the SIRRIPA and a risk-free rate (such as the 10-year U.S. Treasury yield). Through this analytical lens, Rainsy Sam accurately identified a shift in the S&P 500 from undervaluation to overvaluation — anticipating a downturn well before traditional signals caught up. His model demonstrated how declining earnings expectations — fueled by the erratic and destabilizing nature of Trump’s economic measures — would lengthen the PPP, reduce the SIRRIPA, and produce a negative SRP, signaling the market’s slide into bear territory. As financial markets continue to plunge, Rainsy Sam’s analysis underscores the predictive power and practical relevance of the PPP methodology. It affirms its value as a critical instrument for investors, analysts, and policymakers seeking to navigate the complex realities of today’s global economy. (End)

LE PREMIER A AVOIR VU VENIR LE KRACH DE WALL STREET : RAINSY SAM ET LE POUVOIR PREDICTIF DU POTENTIAL PAYBACK PERIOD (PPP) Rainsy Sam — économiste d’origine cambodgienne, analyste financier, gestionnaire de fonds et ancien Ministre des Finances — a été le premier à prédire publiquement le krach actuel de Wall Street, déclenché par les politiques économiques chaotiques du président Donald Trump. Son article du 12 mars, intitulé « Anatomy of a Looming Bear Market: How to Assess the Impact of Donald Trump's Chaotic Economic Measures on Wall Street » (ou « Anatomie d’un krach boursier imminent: Comment évaluer l’impact des mesures économiques chaotiques de Donald Trump sur Wall Street »), a d’abord été publié sur LinkedIn, puis dans la Revue Française d’Économie et de Gestion https://www.revuefreg.fr/index.php/home/article/view/2057/1636, et a rapidement circulé dans les cercles professionnels et financiers. Ce qui distingue cette analyse, c’est l’utilisation du Potential Payback Period (PPP) — un outil d’évaluation révolutionnaire qui va bien au-delà des indicateurs traditionnels comme les ratios P/E et PEG. En intégrant la croissance des bénéfices, les taux d’intérêt et le risque, le PPP permet une compréhension plus rigoureuse, dynamique et prospective de la valorisation des marchés boursiers. Fait important : la prévision de Rainsy Sam ne repose pas sur des notions vagues de "sentiment de marché" ou sur des interprétations subjectives et non chiffrées, comme c’est souvent le cas dans la littérature financière. Elle s’appuie au contraire sur des hypothèses explicites et quantifiées relatives à la croissance future des bénéfices, appuyées par une analyse de sensibilité montrant comment les variations des principales variables influencent le PPP, le SIRRIPA (Stock Internal Rate of Return Including Price Appreciation), et en fin de compte le SRP (Stock Risk Premium), qui représente la différence entre le SIRRIPA et un taux sans risque (tel que le rendement des bons du Trésor américain à 10 ans). Grâce à cette approche analytique, Rainsy Sam a identifié avec précision un basculement du S&P 500 d’une situation de sous-évaluation à une situation de surévaluation — anticipant un retournement bien avant que les signaux traditionnels ne le détectent. Son modèle a démontré comment une baisse des prévisions de bénéfices — alimentée par la nature erratique et déstabilisatrice des mesures économiques de Trump — entraînerait un allongement du PPP, une baisse du SIRRIPA et un SRP négatif, signalant l’entrée du marché en territoire baissier. Alors que les marchés financiers continuent de s’effondrer, l’analyse de Rainsy Sam met en lumière le pouvoir prédictif et la pertinence pratique de la méthodologie PPP. Elle confirme la valeur de cet outil comme instrument essentiel pour les investisseurs, les analystes et les décideurs souhaitant naviguer dans les réalités complexes de l’économie mondiale contemporaine. (Fin)

No international financial journal has accepted to publish any of my articles on the Potential Payback Period (PPP) and its applications because I could not cite any book in my references that had previously discussed the concept. This is unsurprising, as I am the one who developed this new framework, and no one else has yet written a book explaining the PPP, along with its derivatives such as the Stock’s Internal Rate of Return and the Hidden Value Zone, or its various applications. This situation creates a vicious cycle that obstructs the dissemination of innovation—until my book, the first on the subject, is hopefully published in a few months. Until then, the lack of prior literature prevents academic validation, and the absence of validation, in turn, discourages publication. This paradox highlights the difficulties of introducing groundbreaking financial methodologies within the rigid framework of traditional academic publishing.

Abstract: Traditional valuation metrics such as the Price-to-Earnings (P/E) ratio, PEG ratio, and Earnings Yield are widely used in assessing stock and market valuations. However, these tools often lead to misleading conclusions by failing to incorporate earnings growth, discount rates, and risk. The Potential Payback Period (PPP) and its derived Internal Rate of Return (IRR) offer a superior framework by addressing these limitations. This article demonstrates how the PPP and IRR provide a more accurate valuation of the S&P 500 as of January 2025 and explain why a stock with a high P/E ratio can be a better investment than one with a low P/E ratio. The findings challenge conventional wisdom, highlighting the importance of a dynamic, growth-adjusted, and risk-inclusive approach to stock valuation. Keywords: Stock Valuation, Price-to-Earnings (P/E) Ratio, Potential Payback Period (PPP), Internal Rate of Return (IRR), PEG Ratio, Earnings Yield.

Introduction

Stock valuation is a critical aspect of investment decision-making. Traditional metrics like the P/E ratio,

PEG ratio, and Earnings Yield have been widely used for decades, but they fail to capture the full

complexity of stock pricing. By ignoring key factors such as earnings growth, risk, and the cost of capital,

these metrics often lead to erroneous conclusions. This article introduces an alternative framework based on

the Potential Payback Period (PPP) and the Internal Rate of Return (IRR), which offer a more comprehensive

and mathematically sound approach to valuation.

1. The Limitations of Traditional Metrics

Traditional valuation metrics have inherent weaknesses:

• P/E Ratio: Ignores earnings growth and the time value of money,

leading to

misleading comparisons across

companies and industries.

• PEG Ratio: Uses a simplistic linear adjustment that fails to

reflect the real

impact of earnings growth on

valuation.

• Earnings Yield: Provides an incomplete picture of valuation by

neglecting the

interplay between earnings

growth and risk.

These shortcomings are particularly problematic in dynamic market conditions, where earnings growth and

interest rates play a crucial role in determining stock prices. As a result, investors relying solely on

traditional metrics may miss valuable investment opportunities or misinterpret market signals.

2. The Concepts and Formulas Behind the Potential Payback Period (PPP) and the Internal Rate of

Return (IRR)

To address the limitations of traditional metrics, the PPP and IRR introduce a framework that accounts for

earnings growth and risk-adjusted discounting. This section explores the relevance and mathematical

foundation of these two concepts and how they provide a more holistic view of stock valuation.

2.1. The Potential Payback Period (PPP)

The PPP calculates the theoretical number of years required for the cumulative discounted future earnings of

a stock to equal its current price. The formula is as follows:

This formula dynamically adjusts the P/E ratio to reflect the effects of earnings growth and the time value

of money. When growth and interest rates are zero (g = r = 0), the PPP simplifies to the P/E ratio,

demonstrating that the latter is a static case of the more comprehensive PPP framework.

2.2. The Internal Rate of Return (IRR)

The IRR is derived from the PPP and represents the implied annualized return an investor would earn if they

held a stock for a duration equal to its PPP. The formula is:

This formula dynamically adjusts the P/E ratio to reflect the effects of earnings growth and the time value

of money. When growth and interest rates are zero (g = r = 0), the PPP simplifies to the P/E ratio,

demonstrating that the latter is a static case of the more comprehensive PPP framework.

2.2. The Internal Rate of Return (IRR)

The IRR is derived from the PPP and represents the implied annualized return an investor would earn if they

held a stock for a duration equal to its PPP. The formula is:

Unlike traditional metrics, the IRR provides a dynamic, risk-adjusted view of expected returns, making it a

superior tool for evaluating investment opportunities.

3. The S&P 500 Is NOT Overvalued as of January 2025

Despite concerns about high valuations, the PPP and IRR suggest that the S&P 500 remains fairly valued when

earnings growth and risk are taken into account.

3.1. Traditional Metrics Suggest Overvaluation

• P/E Ratio: The S&P 500's P/E of 30 is significantly higher than

its historical average of 16-18, raising

concerns of overvaluation.

• PEG Ratio: With an EPS growth rate of 18%, the PEG ratio is 1.67,

exceeding the conventional threshold of 1.

• Earnings Yield: At 3.33%, it is lower than the risk-free rate of

4.62%, further suggesting overvaluation.

3.2. PPP and IRR Provide a More Accurate Picture

Using PPP and IRR calculations:

• At a 4.62% Discount Rate (Risk-Free Rate):

◦ PPP = 13.10 years

◦ IRR = 5.43%

◦ Since IRR > Risk-Free Rate, the S&P 500 is not overvalued.

• At a 7.62% Discount Rate (Risk-Free Rate + Market Risk Premium):

◦ PPP = 14.76 years

◦ IRR = 4.81%

◦ Still higher than the risk-free rate, justifying current market

levels.

Thus, the S&P 500 remains an attractive investment under both risk-free and risk-adjusted perspectives.

4. High P/E Stocks Can Outperform Low P/E Stocks

4.1. P/E Ratios Can Mislead

Investors often assume that a lower P/E ratio indicates a better investment opportunity. However, this

perspective ignores key factors such as earnings growth and discounting. A stock with a high P/E ratio can

still offer superior returns if its growth rate justifies its valuation.

A real-world comparison between Applied Materials (AMAT) and Broadcom (AVCO), based on data as of January

24, 2025, illustrates this principle.

• Applied Materials (AMAT) has a P/E ratio of 22, which appears

more attractive than Broadcom’s P/E ratio of

188 when considering only this metric. However, stock performance tells a different story.

• Over the last six months:

◦ Applied Materials’ stock price declined by 15%, despite its lower

P/E ratio.

◦ Broadcom’s stock price increased by 50%, despite its high P/E

ratio, highlighting the limitations of static valuation metrics.

4.2. PPP and IRR Tell the Full Story

When earnings growth and discounting are factored in, the comparison between Applied Materials and Broadcom

provides a different perspective:

• Applied Materials (AMAT):

◦ Earnings Growth Rate: 8%

◦ Discount Rate: 4.62%

◦ PPP: 16.89 years

◦ IRR: 4.19%

• Broadcom (AVCO):

◦ Earnings Growth Rate: 32%

◦ Discount Rate: 4.62%

◦ PPP: 16.85 years

◦ IRR: 4.20%

Despite its high P/E ratio, Broadcom’s superior earnings growth results in a PPP and IRR nearly identical to

those of Applied Materials. This demonstrates that Broadcom’s valuation is justified by its strong growth

potential, making it an equally attractive investment.

This analysis reinforces that relying solely on the P/E ratio can be misleading. The PPP and IRR offer a

more comprehensive perspective, incorporating earnings growth and risk-adjusted discounting to provide a

clearer picture of a stock’s true value.

Conclusion

The PPP and IRR offer a more accurate, growth-adjusted valuation framework than traditional metrics.

• For the S&P 500: Despite a historically high P/E ratio, its IRR

remains above the risk-free rate, proving it

is not overvalued.

• For Individual Stocks: Growth-adjusted metrics explain why

high-P/E stocks like Broadcom can outperform low-P/E stocks in the same sector like Applied Materials.

Investors should adopt PPP and IRR for a more accurate understanding of stock valuations. For more

information, visit www.stockinternalrateofreturn.com.

Rainsy Sam

Reference List

1. Basu, S. (1977). Investment performance of common stocks in relation to their price-earnings ratios:

A

test of the efficient market hypothesis. The Journal of Finance, 32(3), 663–682. The article examines

the

behavior of P/E ratios in stock valuation and market performance, providing foundational insight into

their

limitations. Link

2. Bodie, Z., Kane, A., & Marcus, A. J. (2013). Investments (10th ed.). McGraw-Hill. The book offers

comprehensive coverage of investment theory, useful for contrasting traditional valuation methods with

the

PPP-derived IRR.

3. Brealey, R. A., Myers, S. C., & Allen, F. (2020). Principles of Corporate Finance. McGraw-Hill

Education.

The book discusses valuation fundamentals and their practical application in real-world finance.

4. Damodaran, A. (2012). Investment Valuation: Tools and Techniques for Determining the Value of Any

Asset.

Wiley Finance. The book provides an in-depth overview of valuation models, including the P/E ratio and

growth-related metrics, and highlights why traditional methods may fall short in capturing long-term

earning

power.

5. Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal

of

Financial Economics, 33(1), 3-56. The book explores risk factors in stock and bond returns, relevant for

understanding risk-adjusted metrics in investment evaluation.

6. Gordon, M. J., & Shapiro, E. (1956). Capital equipment analysis: The required rate of profit.

Management

Science, 3(1), 102–110. The article is a seminal work on growth models, key to understanding the

discounting

mechanism in PPP and IRR. Link

7. Gordon, M. J. (1962). The Investment, Financing, and Valuation of the Corporation. Irwin Series in

Economics. The book discusses growth models and their impact on corporate valuation.

8. Graham, B., & Dodd, D. (1934). Security Analysis. McGraw-Hill. The book is a classic text on value

investing, emphasizing intrinsic value, a concept central to the PPP framework.

9. Lynch, P., & Rothchild, J. (2000). One Up on Wall Street: How to Use What You Already Know to Make

Money

in the Market. Simon & Schuster. The book discusses practical valuation tools like the PEG ratio and

highlights their limitations in high-growth scenarios.

10. Malkiel, B. G. (2019). A Random Walk Down Wall Street: The Time-Tested Strategy for Successful

Investing. W. W. Norton & Company. The book highlights the importance of advanced valuation methods in

dynamic markets.

11. Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance, and the theory of

investment. The American Economic Review, 48(3), 261-297. The article represents a foundational work in

financial theory, discussing the impact of capital costs on corporate finance decisions, relevant to the

PPP's incorporation of discount rates.

12. Morningstar, Inc. (2024). Key Metrics for Stock Valuation: P/E, PEG, and Beyond. Morningstar

Research

Reports. The report explores modern adaptations of valuation metrics and their use in high-growth

sectors.

13. Piotroski, J. D. (2000). Value investing: The use of historical financial statement information to

separate winners from losers. Journal of Accounting Research, 38, 1-41. The article investigates

alternative

frameworks for stock value assessment.

14. Sam, R. (1984). Le P.E.R., un instrument mal adapté à la gestion mondiale des portefeuilles. Comment

remédier à ses lacunes. Analyse Financière, 2ème trimestre. The article critiques the P/E ratio's

effectiveness in global portfolio management and introduces the "Délai de Recouvrement (DR)" or "Payback

Period (PP)" concept. Link

15. Sam, R. (1985). Le Délai de Recouvrement (DR). Analyse Financière, 3ème trimestre. The article

refines

the DR concept, laying the groundwork for the Potential Payback Period (PPP). Link

16. Sam, R. (1988). Le DR confronté à la réalité des marchés financiers. Analyse Financière, 4ème

trimestre.

The article demonstrates early applications of the DR to portfolio management. Link

17. Sam, R. (2024). Stock Evaluation: Discovering the Potential Payback Period (PPP) as a Dynamic P/E

Ratio.

The website is a dedicated platform for financial analysis, focusing on the PPP's innovative application

in

deriving the IRR. Link

18. Sam, R. (2024). The Potential Payback Period (PPP): Revolutionizing Stock Valuation. [Manuscript in

Progress]. The book will explore the PPP methodology's theoretical foundation and practical

applications.

19. Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk.

The

Journal of Finance, 19(3), 425–442. The article introduces the Capital Asset Pricing Model (CAPM),

essential

for understanding risk adjustments in the PPP. Link

Unlike traditional metrics, the IRR provides a dynamic, risk-adjusted view of expected returns, making it a

superior tool for evaluating investment opportunities.

3. The S&P 500 Is NOT Overvalued as of January 2025

Despite concerns about high valuations, the PPP and IRR suggest that the S&P 500 remains fairly valued when

earnings growth and risk are taken into account.

3.1. Traditional Metrics Suggest Overvaluation

• P/E Ratio: The S&P 500's P/E of 30 is significantly higher than

its historical average of 16-18, raising

concerns of overvaluation.

• PEG Ratio: With an EPS growth rate of 18%, the PEG ratio is 1.67,

exceeding the conventional threshold of 1.

• Earnings Yield: At 3.33%, it is lower than the risk-free rate of

4.62%, further suggesting overvaluation.

3.2. PPP and IRR Provide a More Accurate Picture

Using PPP and IRR calculations:

• At a 4.62% Discount Rate (Risk-Free Rate):

◦ PPP = 13.10 years

◦ IRR = 5.43%

◦ Since IRR > Risk-Free Rate, the S&P 500 is not overvalued.

• At a 7.62% Discount Rate (Risk-Free Rate + Market Risk Premium):

◦ PPP = 14.76 years

◦ IRR = 4.81%

◦ Still higher than the risk-free rate, justifying current market

levels.

Thus, the S&P 500 remains an attractive investment under both risk-free and risk-adjusted perspectives.

4. High P/E Stocks Can Outperform Low P/E Stocks

4.1. P/E Ratios Can Mislead

Investors often assume that a lower P/E ratio indicates a better investment opportunity. However, this

perspective ignores key factors such as earnings growth and discounting. A stock with a high P/E ratio can

still offer superior returns if its growth rate justifies its valuation.

A real-world comparison between Applied Materials (AMAT) and Broadcom (AVCO), based on data as of January

24, 2025, illustrates this principle.

• Applied Materials (AMAT) has a P/E ratio of 22, which appears

more attractive than Broadcom’s P/E ratio of

188 when considering only this metric. However, stock performance tells a different story.

• Over the last six months:

◦ Applied Materials’ stock price declined by 15%, despite its lower

P/E ratio.

◦ Broadcom’s stock price increased by 50%, despite its high P/E

ratio, highlighting the limitations of static valuation metrics.

4.2. PPP and IRR Tell the Full Story

When earnings growth and discounting are factored in, the comparison between Applied Materials and Broadcom

provides a different perspective:

• Applied Materials (AMAT):

◦ Earnings Growth Rate: 8%

◦ Discount Rate: 4.62%

◦ PPP: 16.89 years

◦ IRR: 4.19%

• Broadcom (AVCO):

◦ Earnings Growth Rate: 32%

◦ Discount Rate: 4.62%

◦ PPP: 16.85 years

◦ IRR: 4.20%

Despite its high P/E ratio, Broadcom’s superior earnings growth results in a PPP and IRR nearly identical to

those of Applied Materials. This demonstrates that Broadcom’s valuation is justified by its strong growth

potential, making it an equally attractive investment.

This analysis reinforces that relying solely on the P/E ratio can be misleading. The PPP and IRR offer a

more comprehensive perspective, incorporating earnings growth and risk-adjusted discounting to provide a

clearer picture of a stock’s true value.

Conclusion

The PPP and IRR offer a more accurate, growth-adjusted valuation framework than traditional metrics.

• For the S&P 500: Despite a historically high P/E ratio, its IRR

remains above the risk-free rate, proving it

is not overvalued.

• For Individual Stocks: Growth-adjusted metrics explain why

high-P/E stocks like Broadcom can outperform low-P/E stocks in the same sector like Applied Materials.

Investors should adopt PPP and IRR for a more accurate understanding of stock valuations. For more

information, visit www.stockinternalrateofreturn.com.

Rainsy Sam

Reference List

1. Basu, S. (1977). Investment performance of common stocks in relation to their price-earnings ratios:

A

test of the efficient market hypothesis. The Journal of Finance, 32(3), 663–682. The article examines

the

behavior of P/E ratios in stock valuation and market performance, providing foundational insight into

their

limitations. Link

2. Bodie, Z., Kane, A., & Marcus, A. J. (2013). Investments (10th ed.). McGraw-Hill. The book offers

comprehensive coverage of investment theory, useful for contrasting traditional valuation methods with

the

PPP-derived IRR.

3. Brealey, R. A., Myers, S. C., & Allen, F. (2020). Principles of Corporate Finance. McGraw-Hill

Education.

The book discusses valuation fundamentals and their practical application in real-world finance.

4. Damodaran, A. (2012). Investment Valuation: Tools and Techniques for Determining the Value of Any

Asset.

Wiley Finance. The book provides an in-depth overview of valuation models, including the P/E ratio and

growth-related metrics, and highlights why traditional methods may fall short in capturing long-term

earning

power.

5. Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal

of

Financial Economics, 33(1), 3-56. The book explores risk factors in stock and bond returns, relevant for

understanding risk-adjusted metrics in investment evaluation.

6. Gordon, M. J., & Shapiro, E. (1956). Capital equipment analysis: The required rate of profit.

Management

Science, 3(1), 102–110. The article is a seminal work on growth models, key to understanding the

discounting

mechanism in PPP and IRR. Link

7. Gordon, M. J. (1962). The Investment, Financing, and Valuation of the Corporation. Irwin Series in

Economics. The book discusses growth models and their impact on corporate valuation.

8. Graham, B., & Dodd, D. (1934). Security Analysis. McGraw-Hill. The book is a classic text on value

investing, emphasizing intrinsic value, a concept central to the PPP framework.

9. Lynch, P., & Rothchild, J. (2000). One Up on Wall Street: How to Use What You Already Know to Make

Money

in the Market. Simon & Schuster. The book discusses practical valuation tools like the PEG ratio and

highlights their limitations in high-growth scenarios.

10. Malkiel, B. G. (2019). A Random Walk Down Wall Street: The Time-Tested Strategy for Successful

Investing. W. W. Norton & Company. The book highlights the importance of advanced valuation methods in

dynamic markets.

11. Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance, and the theory of

investment. The American Economic Review, 48(3), 261-297. The article represents a foundational work in

financial theory, discussing the impact of capital costs on corporate finance decisions, relevant to the

PPP's incorporation of discount rates.

12. Morningstar, Inc. (2024). Key Metrics for Stock Valuation: P/E, PEG, and Beyond. Morningstar

Research

Reports. The report explores modern adaptations of valuation metrics and their use in high-growth

sectors.

13. Piotroski, J. D. (2000). Value investing: The use of historical financial statement information to

separate winners from losers. Journal of Accounting Research, 38, 1-41. The article investigates

alternative

frameworks for stock value assessment.

14. Sam, R. (1984). Le P.E.R., un instrument mal adapté à la gestion mondiale des portefeuilles. Comment

remédier à ses lacunes. Analyse Financière, 2ème trimestre. The article critiques the P/E ratio's